In the larger context of bank management and financial services, the book describes a competitive landscape where traditional banks are no longer the sole providers of financial solutions, facing intense rivalry from both nonbank financial firms and giant industrial or retailing corporations. This competition has led to a significant erosion of banks’ market share; while banks once accounted for over two-thirds of all financial-service assets in the U.S. a century ago, that share fell to about one-fifth (18.4%) by 2007.

Primary Nonbank Financial Competitors

The book identifies several key financial institutions that wrestle with banks for customer loyalty by offering similar services:

- Savings Associations and Credit Unions: These depository institutions specialize in home mortgages, household credit, and member-focused savings and loans.

- Money Market and Mutual Funds: These firms pool public savings to invest in short-term liquid assets or professionally managed portfolios of stocks and bonds.

- Hedge Funds: These upscale, lightly regulated investment partnerships attract wealthy investors by supporting a broad, often risky, group of assets.

- Security Brokers, Dealers, and Investment Banks: These firms provide professional advice, execute security trades, and underwrite new issues of stocks and bonds to raise funds for corporations and governments.

- Finance Companies: Institutions like GE Capital or Household Finance offer loans to both commercial enterprises and individuals, typically using funds borrowed in the open market.

- Insurance Companies: Life and property/casualty insurers compete by offering risk protection, managing pension plans, and providing retirement funds.

Retailing and Industrial “Invaders”

The book highlights a growing trend of nonfinancial firms entering the financial marketplace to capture customers:

- General Electric (GE): Through GE Commercial Finance and GE Money, this industrial giant provides loans, leasing, and credit cards to millions worldwide.

- GMAC Financial Services: Originally a captive finance company for General Motors, it evolved into a family of firms offering auto financing, home mortgages, and banking through GMAC Bank.

- Wal-Mart: As the world’s largest retailer, it has aggressively expanded into check cashing, money transfers, and bill payments through in-store “Money Centers,” targeting lower- to middle-income consumers.

Strategic Trends: Convergence and the “Financial Department Store”

A dominant theme in the book is convergence, where industry boundaries have blurred, and different firms now offer many of the same products. This has resulted in the rise of “financial department stores” or “universal banks“—conglomerate financial holding companies (FHCs) that unify banking, insurance, and security brokerage under one corporate umbrella.

Regulatory Context and Management Response

The book notes that much of this competition was enabled by the Gramm-Leach-Bliley (GLB) Act of 1999, which tore down legal barriers separating banking from other financial businesses. Successful management in this environment requires a “market-driven” and “sales-oriented” approach, as financial firms must now compete on price, convenience, and a widening menu of fee-based services to maintain profitability and protect their capital base.

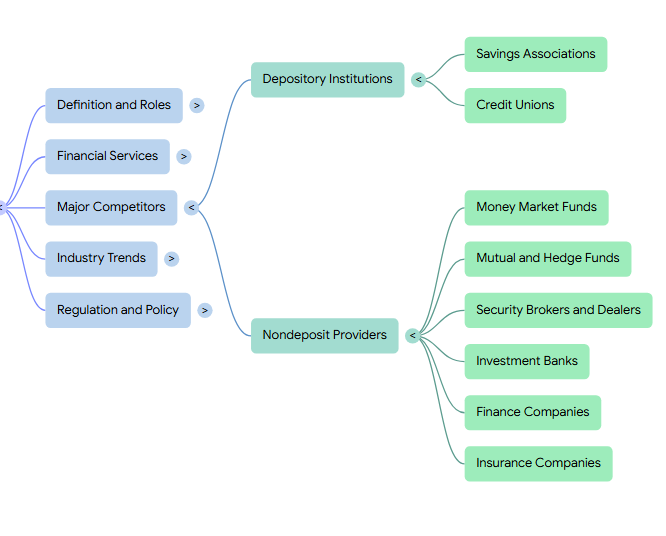

Depository Institutions

In the larger context of major competitors, the book identifies depository institutions as a primary category of financial-service providers that includes commercial banks, savings associations (thrifts), and credit unions. While commercial banks have historically dominated the financial system, they now face intense rivalry from other depository and nondepository firms that offer nearly identical services.

Types of Depository Institutions as Competitors

The book categorizes the main depository competitors as follows:

- Commercial Banks: These are the largest group, selling deposits and making loans to both businesses and individuals. They represent about one-fifth (18.4%) of all U.S. financial assets.

- Savings Associations (Thrifts): These institutions, including savings and loan associations and savings banks, specialize in selling savings deposits and granting home mortgages and other household credit. They were created to encourage family savings and home ownership and have recently expanded their consumer service menus to mirror those of commercial banks.

- Credit Unions: These are nonprofit associations of individuals sharing a “common bond” (such as the same employer). They collect deposits from and make loans only to their members.

The Competitive Landscape

The book emphasizes that the distinction between these institutions has blurred significantly:

- Convergence of Services: As industry boundaries have “come tumbling down,” savings associations and credit unions have moved to capture traditional banking markets such as checkable deposits and small business loans.

- Market Share Erosion: A century ago, banks accounted for more than two-thirds of all financial-service assets in the United States, but that share has fallen to approximately 18.4% as of 2007. Savings institutions and credit unions combined held about 4.5% of total financial assets in the same period.

- Regulatory Parity: Legislation like the Garn-St Germain Depository Institutions Act of 1982 made bank and nonbank depository institutions more alike by giving thrifts new service powers to compete more fully with commercial banks.

Shared Challenges and Risks

Despite their competition, all depository institutions share similar fundamental roles and risks:

- Intermediation Role: They all perform the vital task of acting as a bridge between surplus-spending units (savers) and deficit-spending units (borrowers).

- Liquidity and Safety: Most of these institutions are “insured,” meaning they have chosen to apply for federal insurance (such as through the FDIC or the National Credit Union Share Insurance Fund) to reassure the public.

- Vulnerability: They all face significant maturity mismatches, borrowing short-term cash from the public while extending long-term credit, which creates substantial liquidity and interest-rate risk.

Ultimately, the book suggests that while commercial banks remain the most important gatherers and dispensers of financial information, their survival depends on competing effectively with these other depository “major competitors” on the basis of price, convenience, and service variety.

Savings Associations

In the larger context of depository institutions, the book describes savings associations (often referred to as thrifts) as specialized firms that traditionally focus on attracting household savings and providing credit for home mortgages and other consumer needs. While they were originally established with a narrow mission to encourage family savings and facilitate homeownership, they have evolved significantly through deregulation to become major competitors of commercial banks.

Core Role and Functions

Within the category of depository institutions, which also includes commercial banks and credit unions, savings associations play a vital role in the financial system by:

- Encouraging Savings: They attract a large proportion of the public’s savings, typically through selling relatively small savings accounts.

- Providing Housing Credit: Their primary lending focus is granting home mortgage loans and other forms of household credit to individuals and families.

- Economic Intermediation: Like all depository institutions, they act as a bridge between “surplus-spending units” (savers) and “deficit-spending units” (borrowers), helping to accelerate economic growth.

Convergence and Deregulation

The book emphasizes that the distinction between savings associations and commercial banks has blurred due to a trend known as convergence. Since the government deregulation of the 1980s, savings associations have expanded their service menus to mirror many of those offered by commercial banks, such as offering checking accounts and a wider array of consumer loans. This shift was intended to allow thrifts to remain competitive as the financial-services marketplace became more crowded.

Regulatory and Insurance Framework

Savings associations operate under a specific regulatory structure designed to protect the public’s deposits:

- Supervision: Federally chartered savings associations fall under the jurisdiction of the Office of Thrift Supervision (OTS), a bureau within the U.S. Treasury Department, while state-chartered associations are overseen by state boards or commissions.

- Deposit Insurance: Their deposits were historically insured by the Savings Association Insurance Fund (SAIF), administered by the FDIC. However, under the FDIC Reform Act of 2005, this fund was merged with the Bank Insurance Fund (BIF) to create a single Deposit Insurance Fund (DIF) covering both savings associations and commercial banks.

- Membership: Like banks, they can be wholly or partially owned by holding companies and can even exist as “virtual banks” that operate exclusively over the Internet.

Market Position and Performance

As of 2007, savings institutions held approximately $1,793 billion in financial assets, representing about 3.2% of the total assets in the U.S. financial marketplace. The book notes that while they are generally profitable, FDIC-insured savings associations have recently reported slightly lower asset and equity returns compared to commercial banks. For instance, in early 2007, savings associations averaged a return on assets (ROA) of 0.97 percent, compared to 1.24 percent for commercial banks. Despite this, they remain essential components of the depository industry, providing specialized credit and savings options to millions of households.

Credit Unions

In the larger context of depository institutions, the book describes credit unions as nonprofit associations of individuals who share a “common bond,” such as working for the same employer or belonging to the same organization. Along with commercial banks and savings associations, they form the primary categories of financial-service providers that perform the vital role of financial intermediation—collecting deposits to fund loans.

Core Characteristics and Roles

Within the depository industry, credit unions are unique because of their nonprofit, member-owned structure. Historically, their mission was to provide small savings accounts and low-cost credit to industrial workers, a market often ignored by early commercial banks. Today, their principal functions remain:

- Member-Focused Lending: They collect deposits from and make loans only to their members.

- Intermediation: Like all depository institutions, they act as a bridge between “surplus-spending units” (savers) and “deficit-spending units” (borrowers).

- Risk Balancing: To counterbalance the risks of lending to members, they must maintain sizable investments in government securities, insured bank CDs, and other short-term money market instruments.

Convergence and Competition

A major theme in the book is convergence, where the once-distinct boundaries between depository institutions are blurring. Credit unions have aggressively expanded their service menus to include offerings once exclusive to commercial banks, such as:

- Share Draft Accounts: These function as checkable (transaction) deposits.

- Diversified Credit: They now compete for a growing share of consumer installment credit and small business loans.

- Modern Services: They offer a variety of payments services, including credit and debit cards and Internet-based payment systems.

Regulatory and Insurance Framework

As part of the heavily regulated depository sector, credit unions are “vested with the public interest” and subject to specific oversight:

- Supervision: Federal credit unions are supervised and examined by the National Credit Union Administration (NCUA), while state-chartered units fall under state boards or commissions.

- Insurance: Member deposits are typically insured up to $100,000 (with temporary increases to $250,000) by the National Credit Union Share Insurance Fund.

- Tax Status: Unlike commercial banks, credit unions are generally tax-exempt.

Market Position and Recent Trends

While credit unions are numerous, they represent a smaller portion of the total financial marketplace compared to commercial banks. As of early 2007, they held approximately $741 billion in assets, or about 1.3% of the total assets in the U.S. financial marketplace. The book notes that many credit unions are currently taking advantage of more liberal rules to convert into stockholder-owned depository institutions to attract more capital and gain greater flexibility in their lending and investment activities.

Nondeposit Providers

In the larger context of major competitors, the book identifies nondeposit providers as a diverse and powerful group of financial and nonfinancial firms that wrestle with traditional banks for the loyalty of the public’s savings and credit business. These institutions have significantly eroded the market share of commercial banks, which saw their portion of total U.S. financial assets fall from over two-thirds a century ago to approximately 18.4 percent by 2007.

Principal Nondeposit Financial Competitors

The book categorizes the primary nondeposit financial institutions as follows:

- Mutual Funds (Investment Companies): These firms pool savings from the public to invest in professionally managed portfolios of stocks, bonds, and other securities. They often offer higher prospective yields than conventional bank deposits, attracting significant funds away from traditional banks.

- Money Market Funds: A specialized type of mutual fund that collects short-term, liquid funds from individuals and institutions to invest in high-quality, short-duration securities.

- Life and Property/Casualty Insurance Companies: These firms protect against risks to persons or property while also managing pension plans for businesses and retirement funds for individuals.

- Pension Funds: Both private and government-run funds serve as major repositories for long-term savings, competing directly with bank-offered retirement accounts.

- Security Brokers, Dealers, and Investment Banks: These firms provide professional advice, execute security trades, and underwrite new issues of stocks and bonds to help corporations and governments raise capital.

- Finance Companies: Institutions like GE Capital offer loans to commercial enterprises and individuals using funds primarily borrowed in the open market rather than from deposits.

- Hedge Funds: Private investment partnerships that attract funds from wealthy investors to support a broad and often risky group of assets, such as commodities and real estate.

Nonfinancial “Invaders”

The book highlights that competition for nondeposit services also comes from giant industrial and retailing firms that have entered the financial marketplace:

- General Electric (GE): Through its businesses, GE Commercial Finance and GE Money, this industrial giant provides loans, operating leases, and credit cards to millions of individuals and businesses worldwide.

- Wal-Mart: Although not a bank, this retailing giant has aggressively expanded into financial services—such as check cashing, money transfers, and bill payments—through in-store “Money Centers” targeting lower- to middle-income consumers.

Strategic Context: Convergence and the “Financial Department Store”

A dominant theme in the book is convergence, the trend of different types of financial-service providers invading each other’s traditional territory. This has led to the rise of “financial department stores” or “universal banks“—conglomerate financial holding companies (FHCs) that unify banking, insurance, and security brokerage services under one corporate umbrella.

Legislation like the Gramm-Leach-Bliley Act (1999) enabled this environment by tearing down the regulatory walls that once separated these various nondeposit providers from the banking industry. As a result, the book notes that it is increasingly difficult for the public to separate banks from their nondeposit competitors, as nearly all major players now offer similar menus of credit, savings, payments, and risk protection services.

Money Market Funds

In the larger context of nondeposit providers, the book identifies money market funds (MMFs) as a specialized type of mutual fund that competes aggressively with traditional banks for the public’s savings. These institutions collect short-term, liquid funds from individuals and institutions to invest in high-quality, short-duration money market securities.

Functions and Competitive Role

As nondeposit providers, MMFs are characterized by the following roles and impacts:

- Professional Cash Management: Surfacing in the 1970s, MMFs were designed to offer professional cash management services to both households and institutions.

- Market Share Rivalry: MMFs often offer higher prospective yields than conventional bank deposits, which has allowed them to attract a significant volume of funds away from traditional banks. The book notes that this intense competition eventually helped spur government deregulation of the banking industry.

- Asset Volume: As of early 2007, money market funds held approximately $2,390 billion in total financial assets, representing about 4.3 percent of all financial assets held in the United States.

Investment Criteria and Pricing

To maintain their status as low-risk nondeposit alternatives, MMFs adhere to strict investment guidelines. Their assets must be dollar-denominated with remaining maturities of no more than 397 days, and they must maintain a dollar-weighted average maturity of no more than 90 days. A key objective for these funds is to keep their share prices fixed at a standard of $1.00 per share.

Regulation and Risk

While MMFs are nondeposit providers, they are subject to specific oversight and faced unique challenges during recent financial turmoil:

- Regulatory Oversight: The chief regulator for MMFs in the United States is the Securities and Exchange Commission (SEC), which requires these businesses to submit periodic financial reports and provide investors with a prospectus.

- Crisis Response: In the wake of the 2007–2008 credit crisis, the U.S. Treasury made federal insurance available to MMFs to calm public concerns and maintain stable share prices.

- “Breaking the Buck”: The book highlights that despite their relative safety, interest rate risk can impact these funds; during the 2008 crisis, a few money market funds were forced to “break the buck,” meaning their net asset value fell below the $1.00 per share standard.

Mutual and Hedge Funds

In the larger context of nondeposit providers, the book identifies mutual funds and hedge funds as powerful financial institutions that compete directly with traditional banks for the public’s savings and investment business. These entities are part of a diverse group of nondeposit financial institutions that have significantly eroded the market share of commercial banks over the past century.

Mutual Funds (Investment Companies)

The book describes mutual funds as professionally managed investment programs that pool savings from the public to acquire a diversified portfolio of stocks, bonds, and other securities.

- Historical and Competitive Role: While they originated in Belgium in 1822, mutual funds became a major competitor to U.S. banks during the 1920s. They are highly successful at attracting funds away from banks by offering the prospect of higher yields, although these products generally carry more risk than insured bank deposits.

- Market Impact: By early 2007, investment companies (mutual funds) held approximately 13.2 percent of all financial assets in the United States, representing more than $7 trillion in assets.

- Regulation: Mutual funds face close federal and state regulation, primarily by the Securities and Exchange Commission (SEC), which requires them to register, submit periodic financial reports, and provide investors with a detailed prospectus.

Hedge Funds

The book characterizes hedge funds as a more recent and aggressive alternative to mutual funds, designed to provide high returns through specialized investment strategies.

- Target Audience and Strategy: Unlike mutual funds, which serve the general public, hedge funds typically sell shares to “upscale” or wealthy investors. They invest in a broad and often risky array of assets, including commodities, real estate, and loans to distressed companies, and frequently utilize significant leverage (debt) to boost returns.

- Regulatory Status: Hedge funds are noted for being among the most lightly regulated financial institutions because they traditionally do not seek funds from small investors who require extra protection. The book indicates that they are generally subject to no government restrictions on trading activities, registration, or debt usage.

Context of Convergence and Competition

Within the broader financial services landscape, both mutual and hedge funds are central to the trend of “convergence,” where industry boundaries blur and different firms offer similar products. The book explains that many leading banks and financial conglomerates now function as “financial department stores,” owning their own mutual fund and hedge fund affiliates to provide customers with “one-stop shopping” for credit, savings, and investment needs. This rise of nondeposit providers has forced traditional banks to develop their own modern investment services to remain competitive and protect their capital base.

Security Brokers and Dealers

In the larger context of nondeposit providers, the book identifies security brokers and dealers as a leading category of financial-service institutions that compete directly with banks for the public’s savings and investment business. These firms have been central to the trend of industry convergence, as they move into traditional banking territories while banks simultaneously expand into the securities business.

Role and Core Services

According to the book, security brokers and dealers serve as intermediaries that buy and sell securities (such as stocks and bonds) on behalf of their customers and for their own accounts. Their primary functions in the economy include:

- Security Brokerage: Executing buy and sell orders for trading customers.

- Investment Banking (Underwriting): Assisting corporations and governments in raising new funds by purchasing new issues of securities and reselling them to investors.

- Financial Advising: Providing professional guidance on market conditions, mergers, acquisitions, and capital-raising strategies.

Competition and Convergence

The book notes that these firms have become aggressive competitors to traditional banks by offering parallel services, such as interest-bearing online checkable accounts that often pay higher rates than many banks. This competition was significantly accelerated by the Gramm-Leach-Bliley Act of 1999, which tore down legal barriers and allowed securities firms and banks to affiliate under common ownership through financial holding companies. As a result, many large security firms have chartered their own banks or created insurance affiliates to offer “one-stop shopping” for financial services.

Financial Statement Characteristics

The financial statements of security brokers and dealers differ markedly from those of traditional depository institutions. According to the book:

- Assets: Their balance sheets are typically dominated by holdings of corporate stocks, bonds, and money market instruments.

- Liabilities and Equity: They finance these asset acquisitions primarily through borrowings in the money and capital markets and equity capital contributed by their owners.

- Revenues: Income is primarily generated through commissions for buying and selling securities, underwriting fees for assisting businesses with new offerings, and fees for financial advice.

Regulation and Risk

Security brokers and dealers operate under a combination of federal and state supervision. The book identifies the Securities and Exchange Commission (SEC) as the chief federal regulator in the United States. The SEC requires these firms to register, submit periodic financial reports, and limits the volume of debt they can take on. Regulatory focus also includes investigating insider trading and ensuring the accuracy and objectivity of the investment advice provided to clients. Unlike bank deposits, the investment products sold by these firms are generally not insured by the FDIC and are subject to market loss.

Investment Banks

The book categorizes investment banks (IBs) as a primary group of nondeposit providers that compete directly with commercial banks for the fund-raising and advisory business of corporations and governments. Unlike depository institutions, IBs do not rely on traditional customer deposits; instead, they finance their operations primarily through borrowings in the money and capital markets and equity capital contributed by their owners. Their core functions include security underwriting—purchasing new issues of stocks and bonds to resell to investors—and providing expert advice on mergers, acquisitions, and market expansion.

Investment banks have played a significant role in the long-term erosion of commercial banking’s market share, which dropped from over two-thirds of total U.S. financial assets a century ago to approximately 18.4 percent by 2007. The relationship between these institutions was fundamentally altered by the Gramm-Leach-Bliley Act of 1999, which repealed decades-old restrictions and permitted IBs to affiliate with commercial banks and insurance companies under common ownership. This legislative shift allowed for the creation of financial holding companies (FHCs), moving the U.S. financial system toward a “universal banking” model where one firm can meet all of a customer’s financial needs.

Despite the potential for high returns, the book emphasizes that investment banking is substantially more risky and volatile than traditional commercial banking. This volatility was demonstrated during the credit crisis of 2007–2009, which saw the collapse or forced absorption of major firms like Bear Stearns and Lehman Brothers. In response to this instability, remaining industry leaders such as Goldman Sachs and Morgan Stanley transitioned from pure investment banks into commercial bank holding companies to gain access to stable insured deposits and Federal Reserve lending. Consequently, many of the most powerful investment banks today operate as units within massive, diversified financial conglomerates that bridge the gap between traditional banking and global security markets.

Finance Companies

In the larger context of nondeposit providers, the book identifies finance companies as significant financial institutions that compete directly with banks for both business and household credit. Unlike depository institutions, these firms do not rely on customer deposits; instead, they raise loanable funds principally by borrowing in the money and capital markets—such as through the issuance of commercial paper—or by obtaining funds from parent companies.

Core Functions and Market Role

According to the book, the primary role of finance companies is to extend credit to two major segments:

- Commercial Enterprises: They offer loans to businesses, such as automobile and appliance dealers, often to finance inventories (floor planning) or equipment.

- Individuals and Families: They provide household credit for “big-ticket” items like furniture and appliances, as well as personal cash loans.

Financial Statement Characteristics

The financial statements of finance companies reflect their specialized lending focus and unique funding structure:

- Assets: Their balance sheets are dominated by loans, which are typically labeled as “accounts receivable,” including business, consumer, and real estate receivables.

- Liabilities: Because they are nondeposit providers, their “sources of funds” side shows heavy reliance on money market borrowings rather than customer deposits.

Competitive and Strategic Positioning

The book notes that finance companies have significantly eroded the market share of traditional banks in both consumer and business credit markets. This competition is often driven by “nonfinancial invaders”—giant industrial or retailing firms that operate finance company affiliates to support their primary business activities. Notable examples include:

- GE Capital (General Electric): A massive provider of commercial loans, leasing, and credit cards.

- GMAC Financial Services: Originally a “captive” finance company for General Motors, it evolved into a diverse family of firms offering auto financing, home mortgages, and commercial loans.

- HSBC Finance Corporation: Formerly Household International, this is one of the world’s largest consumer lending affiliates, specializing in credit for middle-class borrowers.

Regulatory Framework

Finance companies are primarily regulated at the state government level. State commissions typically focus on:

- The types and contents of loan agreements offered to the public.

- The interest rates charged, with some states setting maximum allowable loan rates.

- The legal methods used to repossess property or recover funds from delinquent borrowers.

The book also highlights that relatively light state regulation has led to a recent explosion of smaller-scale finance companies, such as payday lenders and pawn shops, which often provide small, short-term cash advances at the highest interest rates in the industry.

Insurance Companies

In the larger context of nondeposit providers, the book identifies insurance companies as primary financial institutions that compete directly with banks for the public’s savings and for the management of risk. These firms are a major part of the “nondeposit” sector, which has collectively eroded the market share of traditional commercial banks over the past century.

Core Functions and Types of Insurers

According to the book, insurance companies are generally divided into two main categories:

- Life Insurance Companies: These firms protect individuals and families against financial loss due to death or disability and often include a savings component in their policies. They are also major players in managing business pension plans and individual retirement funds.

- Property/Casualty Insurers: These companies provide risk protection for personal and business property, covering losses from accidents, negligence, storm damage, and other adverse events.

Financial Statement Characteristics

The book notes that the financial statements of insurance companies differ significantly from those of depository institutions.

- Assets: While insurers do make loans, these typically appear on their balance sheets as holdings of corporate stocks, bonds, and mortgages purchased in the open market.

- Liabilities and Funding: Their primary sources of funds are policyholder premium payments and borrowings in the money and capital markets.

- Profitability: Interestingly, the book states that most of the insurance industry’s profits are derived from the investments they make with premium income rather than from the premiums themselves.

Competitive Landscape and Convergence

Insurance companies are central to the trend of convergence, where industry boundaries blur. The book explains that many leading insurers, such as MetLife, State Farm, and Prudential, now own banks or operate through financial holding companies to cross-sell banking and insurance services. Conversely, the Gramm-Leach-Bliley Act of 1999 allowed banks to acquire insurance firms, leading to “one-stop shopping” where a single firm meets all of a customer’s credit, investment, and risk-protection needs.

Regulatory Framework

As nondeposit providers, insurance companies are unique because they are regulated almost exclusively at the state level.

- State Supervision: State insurance commissions prescribe policy content, set maximum premium rates, and license agents.

- Federal Oversight: The federal government becomes involved primarily when insurers sell equity or debt securities to the public (requiring SEC approval) or when they form holding companies to acquire banks (subject to Federal Reserve review).

Performance Indicators

To evaluate the success of these nondeposit providers, the book highlights several unique performance metrics:

- The combined ratio of claims paid plus operating expenses relative to earned premiums.

- The growth of net premiums written (a measure of total sales).

- The size of life and pension reserves relative to total assets.

— Linden Lake

This series:

→ Book Review (1 of 5): Bank Management and Financial Services – Definition and Roles

→ Book Review (2 of 5): Bank Management and Financial Services – Financial Services

→ Book Review (3 of 5): Bank Management and Financial Services – Major Competitors

→ Book Review (4 of 5): Bank Management and Financial Services – Industry Trends

→ Book Review (5 of 5): Bank Management and Financial Services – Regulation and Policy

Leave a Reply