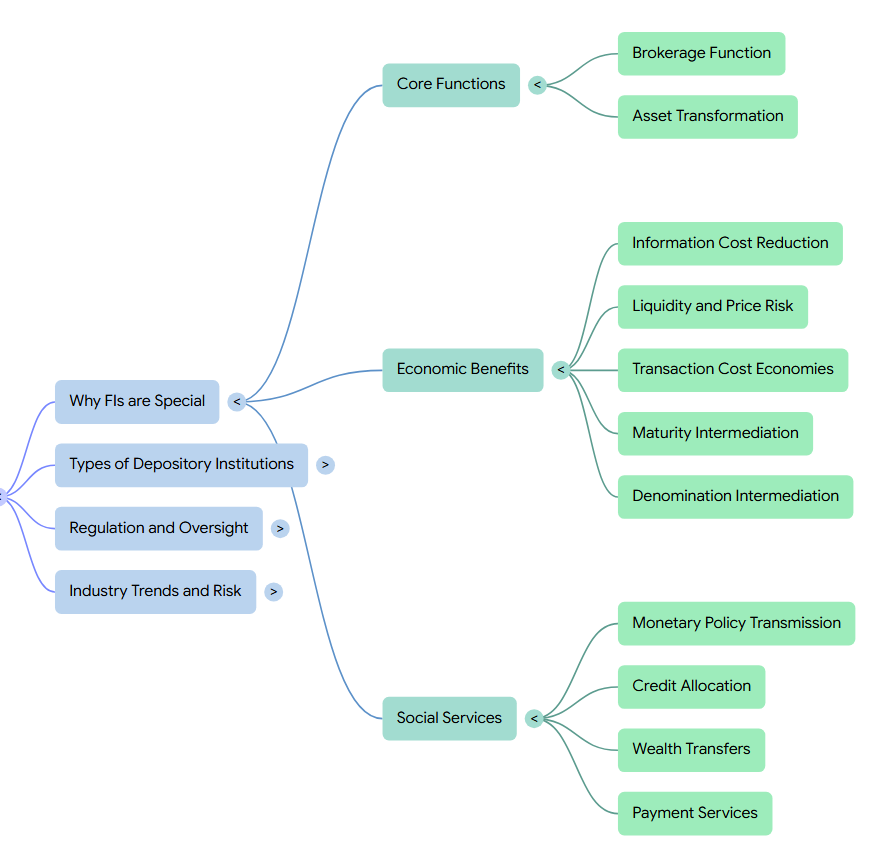

Why Financial Institutions are Special

Financial institutions (FIs) are considered special because they provide essential functions that benefit the economy by channeling funds from those with a surplus to those with a shortage. In a world without FIs, the flow of funds between these groups would be significantly lower due to high monitoring costs, liquidity costs, and price risks. The book identifies several key areas that constitute this “specialness”:

Primary Functions of Specialness

FIs fulfill their special role through two primary functions:

- Brokerage Function: FIs act as agents for savers by providing information and transaction services. This reduces transaction and information costs, encouraging a higher rate of savings.

- Asset-Transformation Function: FIs purchase primary securities (such as corporate bonds and loans) and fund them by issuing secondary securities (such as deposits and insurance policies) that are more attractive to household savers. This adds value by transforming financial risk.

Key Services Provided to Savers

The “specialness” of FIs is further defined by the specific services they offer that individuals cannot easily achieve on their own:

- Information Costs and Delegated Monitoring: FIs act as delegated monitors on behalf of small savers. Because of their size, they have a greater incentive and a lower average cost to collect information and monitor the actions of corporate borrowers.

- Liquidity and Price Risk: FIs provide secondary claims with superior liquidity attributes, such as demand deposits that can be withdrawn immediately. They use diversification and the law of large numbers to offer these low-risk, highly liquid claims while investing in relatively illiquid, higher-risk assets.

- Transaction Cost Services: By grouping assets and purchasing them in bulk, FIs achieve economies of scale that reduce the transaction costs for individual savers.

- Maturity Intermediation: FIs can better bear the risk of mismatching the maturities of their assets (e.g., long-term mortgages) and liabilities (e.g., short-term deposits) than can individual savers.

- Denomination Intermediation: FIs like mutual funds allow small investors to overcome constraints imposed by large minimum denominations of certain assets, such as $250,000 commercial paper.

Systemic and Social Aspects of Specialness

Beyond individual services, FIs are special due to their role in the broader economy:

- Transmission of Monetary Policy: Depository institutions are the primary conduit through which the Federal Reserve’s monetary policy actions impact the rest of the financial system.

- Credit Allocation: FIs are often the only source of financing for critical sectors such as farming and residential real estate.

- Intergenerational Wealth Transfers: Life insurance companies and pension funds provide the ability to transfer wealth across generations, often aided by special tax treatments.

- Payment Services: The efficiency of payment systems, such as check clearing and wire transfers provided by depository institutions, directly benefits the entire economy.

The Link to Regulation

Because FIs are so vital, their failure can cause negative externalities that cripple the economy, such as bank runs or the destruction of household savings. This special role justifies extensive regulation to ensure safety and soundness, protect consumers and investors, and maintain the smooth operation of the monetary system.

The Changing Dynamics of Specialness

The nature of this specialness is not static. For example, the shift from an “originate and hold” banking model to an “originate to distribute” model (where loans are quickly sold or securitized) has reduced the role of FIs as long-term risk specialists. Furthermore, the rise of shadow banks—non-financial firms performing banking services—has created new competition for traditional FIs. This evolution was a major factor in the financial crisis of the late 2000s, which the book characterizes as a failure of FI specialness.

Financial institutions (FIs) are considered special because they perform core functions that overcome market imperfections, which would otherwise significantly hinder the flow of funds between savers and borrowers. Their primary role is channeling funds from those with a surplus to those with a shortage.

The book categorizes these core functions into two primary roles and several specific services that define their unique position in the economy:

Primary Functional Roles

FIs fulfill their special status through two distinct operational frameworks:

- Brokerage Function: In this role, the FI acts as an agent for the saver, providing information and transaction services. By performing investment research and executing trades more efficiently than individuals, FIs achieve economies of scale that reduce transaction and information costs, ultimately encouraging a higher rate of savings in the economy.

- Asset-Transformation Function: FIs purchase primary securities (like corporate bonds and loans) and fund them by issuing secondary securities (like deposits or insurance policies). This adds value by transforming financial risk, creating products that are more attractive and less risky for household savers than direct investments in corporations.

Specific Functions Enhancing “Specialness”

Beyond these broad roles, FIs provide several specialized functions that individual savers cannot easily replicate:

- Delegated Monitoring: Because of the high cost of collecting information and monitoring borrowers, small savers appoint FIs to act as delegated monitors. FIs have a greater incentive and a lower average cost to monitor corporate actions due to their size and expertise.

- Liquidity and Price Risk Intermediation: FIs offer secondary claims with superior liquidity (such as demand deposits) that can be withdrawn immediately, while investing in relatively illiquid primary assets. They use diversification and the law of large numbers to offer these low-risk claims despite the risky nature of their underlying asset portfolios.

- Maturity Intermediation: FIs can better bear the risk of mismatching the maturities of their assets and liabilities. For example, they can offer long-term fixed-rate mortgages to borrowers while raising funds through short-term deposit contracts.

- Denomination Intermediation: FIs like mutual funds allow small investors to overcome constraints imposed by the large minimum denominations of certain assets, such as $250,000 commercial paper.

- Transaction Cost Services: By grouping assets and purchasing them in bulk, FIs achieve economies of scale that significantly lower transaction costs for individual savers.

Systemic and Social Functions

The book also highlights functions that make FIs special from a broader societal and regulatory perspective:

- Transmission of Monetary Policy: Depository institutions serve as the primary conduit through which the Federal Reserve’s monetary policy actions impact the overall economy.

- Credit Allocation: FIs are often the sole source of financing for critical sectors, such as farming and residential real estate, which are pre-identified as being in special need of support.

- Payment Services: The efficiency of check-clearing and wire transfer systems provided by depository institutions directly benefits the entire economy.

- Intergenerational Wealth Transfers: Life insurance companies and pension funds provide the ability for savers to transfer wealth across generations, often aided by special tax treatments.

The Context of Specialness and Regulation

These core functions are so vital that a breakdown in their efficient provision—such as a bank failure—can impose negative externalities on the entire community, such as destroying household savings or restricting a firm’s access to credit. This unique role justifies the extensive safety and soundness regulation that FIs face, which is designed to protect the economy from such systemic shocks

Brokerage Function

The brokerage function is one of the two primary operational frameworks through which financial institutions (FIs) fulfill their special role in the economy. In this capacity, an FI acts as an agent for the saver, providing vital information and transaction services that bridge the gap between household savers and corporate users of funds.

Roles and Services within the Brokerage Function

When acting as a pure broker, an FI does not transform the securities issued by the net users of funds into different claims; rather, it facilitates the direct transfer of funds at a low cost. The book highlights several key activities:

- Information Production: Full-service securities firms conduct extensive investment research and provide recommendations to their clients.

- Transaction Execution: Brokers execute the purchase or sale of securities for commissions or fees. Discount brokers, for instance, focus on carrying out these trades with greater efficiency and at better prices than individuals could achieve alone.

- Specialized Identification: Independent insurance brokers identify the best policies for household savers to fit their specific retirement and savings plans.

- Advisory Services: This includes assisting in mergers and acquisitions (M&A) by finding partners, assessing values, and recommending terms.

Economic Impact and “Specialness”

The brokerage function is considered “special” because it directly addresses market imperfections that would otherwise discourage savings:

- Reduction of Transaction Costs: By grouping assets and purchasing them in bulk, FIs achieve economies of scale. This reduces the costs of trading and often results in lower bid-ask spreads for individual savers.

- Lowering Information Costs: FIs reduce the expense and effort required for individuals to collect high-quality information about corporate borrowers, which encourages a higher overall rate of savings in the economy.

The Context of Core Functions

In the broader context of FI management, the brokerage function is distinguished from the asset-transformation function. While a broker acts as an intermediary for primary securities (like corporate bonds and stocks), an asset transformer actually purchases those primary securities and funds them by issuing secondary securities (like deposits or insurance policies) that have different risk and liquidity profiles.

Despite this distinction, many modern FIs are structured as financial services holding companies, allowing them to perform both brokerage and asset-transformation functions simultaneously under one corporate umbrella. For example, a large bank may offer traditional deposit accounts (asset transformation) while its securities affiliate provides brokerage services and underwriting.

Asset Transformation

In the context of why financial institutions (FIs) are considered special, the asset-transformation function is one of the two primary operational frameworks through which FIs fulfill their core role in the economy,. While the brokerage function involves FIs acting as agents, the asset-transformation function involves FIs acting as principals by purchasing primary securities (such as corporate bonds, loans, and equities) and funding them by issuing secondary securities (such as deposits and insurance policies),.

The book highlights several key aspects of this function within the larger context of FI management:

The Mechanism of Risk Transformation

FIs act as independent market parties that create financial products whose value added to clients is the transformation of financial risk. By issuing secondary securities that are far more attractive to household savers than the primary claims issued directly by corporations, FIs encourage a higher rate of savings in the economy,. This attractiveness is rooted in the FI’s ability to resolve three specific costs and risks:

- Information Costs and Delegated Monitoring: Individual savers often find it too costly to collect information and monitor corporate borrowers. In their asset-transformation role, FIs act as delegated monitors, using their size and expertise to monitor borrowers at a lower average cost (economies of scale) than individuals could achieve,. For example, shorter-term bank loans allow FIs to exercise more monitoring power and obtain “insider-like” information compared to long-term bonds,.

- Liquidity and Price Risk: FIs provide secondary claims with superior liquidity attributes, such as demand deposits that can be withdrawn immediately, while investing in relatively illiquid primary assets like long-term loans. They use diversification and the “law of large numbers” to offer these low-risk, liquid claims despite the risky and illiquid nature of their underlying asset portfolios.

- Maturity Intermediation: FIs are better equipped than individual savers to bear the risk of mismatching the maturities of their assets and liabilities. They can produce long-term contracts, such as 30-year fixed-rate mortgages, while raising funds through short-term liability contracts,.

- Denomination Intermediation: FIs allow small investors to overcome constraints imposed by the large minimum denominations of certain primary assets (e.g., $250,000 commercial paper) by pooling funds through vehicles like mutual funds,.

Systemic and Social Importance

The asset-transformation function has broader implications for the overall economy:

- Transmission of Monetary Policy: Depository institutions are the primary conduit through which the Federal Reserve’s monetary policy actions impact the financial system, largely because their secondary securities (deposits) are a significant component of the money supply,.

- Credit Allocation: FIs often serve as the sole source of financing for critical sectors, such as farming and residential real estate, by transforming general savings into targeted credit,.

Risks and Changing Dynamics

Performing the asset-transformation function inherently exposes FIs to significant risks, including credit risk (default), interest rate risk (from maturity mismatching), and liquidity risk (from sudden liability withdrawals),.

The book notes that the nature of asset transformation is evolving. Many FIs have shifted from an “originate and hold” model, where they keep transformed assets until maturity, to an “originate to distribute” model,. This latter model involves securitization—packaging and selling loans as new securities—which removes assets from the balance sheet and reduces the FI’s traditional role as a long-term risk specialist,. This shift was a significant factor in the financial crisis of the late 2000s, which is characterized in the book as a failure of FI specialness,.

Economic Benefits

Financial institutions (FIs) are considered special because they provide unique economic benefits that overcome market imperfections, which would otherwise significantly impede the flow of funds between savers and borrowers. These benefits are realized through their core roles as brokers and asset transformers.

Benefits to Household Savers

In a world without FIs, individuals would face high costs and risks that would likely deter them from saving or investing directly in corporate securities. FIs provide several specific economic benefits to mitigate these issues:

- Reduced Information Costs and Delegated Monitoring: Collecting information and monitoring corporate borrowers is costly for individual savers. FIs act as delegated monitors, using their size to achieve economies of scale that lower the average cost of information collection.

- Liquidity and Price Risk Intermediation: FIs offer secondary claims (like demand deposits) that have superior liquidity attributes and lower price risk compared to primary securities (like corporate bonds). They use diversification and the law of large numbers to offer these low-risk claims while investing in a portfolio of risky, relatively illiquid assets.

- Reduced Transaction Costs: By pooling the funds of many small savers and purchasing assets in bulk, FIs achieve economies of scale that significantly lower transaction costs for individual investors.

- Maturity and Denomination Intermediation: FIs are better equipped than individuals to bear the risk of mismatching the maturities of their assets and liabilities, such as offering long-term mortgages funded by short-term deposits. They also provide denomination intermediation, allowing small investors to access high-denomination assets (like $250,000 commercial paper) by pooling their funds in vehicles like mutual funds.

Broad Economic and Systemic Benefits

Beyond individual services, FIs are special because of the essential role they play in the overall health and stability of the economy:

- Transmission of Monetary Policy: Depository institutions are the primary conduit through which the Federal Reserve’s monetary policy actions impact the financial system and the overall economy.

- Efficient Payment Services: The provision of check-clearing and wire transfer services by depository institutions directly benefits the economy by ensuring the smooth flow of funds for transactions.

- Credit Allocation: FIs often serve as the major, and sometimes only, source of financing for critical sectors such as farming and residential real estate, which are socially and economically vital.

- Intergenerational Wealth Transfers: Life insurance companies and pension funds provide the mechanism for savers to transfer wealth across generations, often supported by special tax treatments.

The Context of Regulation

The economic benefits provided by FIs are so vital that a failure to provide them—such as a bank failure—can impose severe negative externalities on the entire community, including the destruction of household savings and restricted access to credit for firms. This unique role and the potential for systemic harm justify the extensive safety and soundness regulation that FIs face, designed to protect the integrity of the financial system.

Information Cost Reduction

One of the primary economic benefits provided by financial institutions (FIs) is the significant reduction of information costs for savers. In a world without FIs, individual households would face prohibitively high costs to collect and monitor information on corporate borrowers, which would likely discourage them from investing directly in corporate securities.

FIs reduce these costs through two core functional roles and by achieving economies of scale:

The Brokerage Function and Information Costs

In their role as brokers, FIs act as agents for savers by providing information and transaction services.

- Efficiency and Expertise: Full-service securities firms and insurance brokers specialize in investment research and identifying products that fit specific customer needs.

- Reduced Friction: By performing these services more efficiently than individuals could on their own, FIs reduce the information “imperfections” between those who have funds (savers) and those who need them (borrowers). This encourages a higher overall rate of savings within the economy.

The Asset-Transformation Function and Delegated Monitoring

When acting as asset transformers, FIs provide a more complex service known as delegated monitoring.

- Centralized Monitoring: Instead of thousands of small savers each attempting to monitor a single firm, they “appoint” an FI to act on their behalf. The FI groups these funds and has a much greater incentive—and a lower average cost—to collect information and monitor the firm’s actions because it has a larger stake in the outcome.

- Proprietary Information: FIs often develop secondary securities, like bank loans, that allow them to monitor more effectively. Short-term bank loans, for example, give the FI the power to frequently update information and gain “insider-like” familiarity with a borrower’s operations.

- Reducing Asymmetry: This centralized production of timely information reduces the information asymmetry between the ultimate suppliers and users of funds in the economy.

Economies of Scale in Information Production

The economic benefit of information cost reduction is largely driven by economies of scale. The book notes that while the cost of an investment report might be high for a small individual investor with only $10,000, that same cost is trivial for an FI managing $10 million. By aggregating funds, FIs can spread the fixed costs of information collection across a large asset base, resulting in a significantly lower average cost per saver.

Broader Economic Context

Beyond individual benefits, the reduction of information costs has systemic economic implications. It facilitates credit allocation to vital sectors like farming and small businesses, which might otherwise be seen as too information-intensive for individual investors to support. Furthermore, these information-based services are so critical that their breakdown—such as during a financial crisis—can lead to a “crisis of confidence” that disrupts the entire financial system. This essential role in maintaining economic efficiency is a primary justification for the extensive safety and soundness regulation that FIs face.

Liquidity and Price Risk

Financial institutions (FIs) provide significant economic benefits by acting as intermediaries that mitigate liquidity and price risk for individual savers, thereby encouraging a higher overall rate of savings in the economy.

Definitions of Liquidity and Price Risk

- Liquidity is defined as the ease with which an asset can be converted into cash at a price that is predictable and close to its fair market value.

- Price Risk refers to the possibility that the sale price of an asset will be lower than its initial purchase price, leading to a capital loss for the investor.

The Disincentives of a World Without FIs

In a hypothetical economy without FIs, household savers would have to invest directly in securities issued by corporations. This creates two major economic disincentives:

- Liquidity Costs: Corporate equity and debt are often relatively long-term. Without a liquid secondary market, households might choose to hold cash rather than invest, especially if they anticipate needing funds for near-term consumption.

- Price Risk Exposure: Even if markets exist for trading these securities, individual investors face the risk that the price they receive upon selling will be significantly different from what they paid, compounded by high transaction costs for small-scale trades.

FIs as Asset Transformers

FIs overcome these market imperfections through their asset-transformation function. They purchase “primary securities” (risky, long-term claims like corporate bonds and loans) and fund them by issuing “secondary securities” (like demand deposits) that have superior liquidity attributes and lower price risk for savers.

Mechanisms for Reducing Risk

The book explains that FIs can credibly promise liquidity while investing in risky, illiquid assets through two main mechanisms:

- Diversification: By exploiting their large size, FIs can diversify away significant amounts of portfolio risk, specifically risk that is unique to individual firms. Research suggests that equal investments in as few as 15 securities can provide substantial diversification benefits.

- The Law of Large Numbers: Large FIs use the law of large numbers to predict expected returns on their asset portfolios more accurately than individual savers can. A domestically and globally diversified FI can generate an almost risk-free return on its assets, allowing it to fulfill promises of high liquidity with little capital value risk to its depositors.

Broader Economic Context

By providing these services, FIs reduce the economic disincentives for individuals to participate in the financial system. This results in an increased flow of funds from savers to borrowers, which supports economic growth. However, because this function is so critical, a breakdown—such as the failure of an FI to provide liquidity—can cause negative externalities that harm the entire community, such as a “crisis of confidence” or a bank run. This vital economic role is a primary justification for the extensive safety and soundness regulation imposed on FIs.

Transaction Cost Economies

Financial institutions (FIs) provide significant economic benefits by offering transaction cost services that exploit economies of scale. These services are a key part of what makes FIs “special” in the financial system because they reduce the costs and risks for individuals who want to invest their savings.

Mechanism of Transaction Cost Economies

FIs achieve transaction cost economies primarily through their size and their ability to aggregate funds from many small savers:

- Economies of Scale: By grouping the assets of many savers together and purchasing assets in bulk, FIs can significantly lower the average transaction cost per individual.

- Lower Trading Costs: Since fixed commissions for small retail buyers are often higher than for large wholesale buyers, FIs like mutual funds and pension funds can use their volume to negotiate better prices and lower commissions.

- Reduced Bid-Ask Spreads: In secondary markets, the “bid-ask” (buy-sell) spreads are normally lower for assets bought and sold in large quantities, a benefit that FIs pass on to their participants.

Larger Context of Economic Benefits

Transaction cost economies are one of several ways FIs provide a net social welfare benefit to the economy. Their ability to reduce these costs directly impacts the flow of funds in the following ways:

- Encouraging Savings: By lowering the “imperfections” and friction in the market (like high fees), FIs encourage a higher rate of overall savings in the economy than would exist if individuals had to trade on their own.

- Overcoming Constraints: FIs provide denomination intermediation, allowing small investors to access high-value assets (such as $250,000 commercial paper) by pooling funds, which would otherwise be cost-prohibitive for an individual.

- Providing Liquidity: Because FIs can transact more efficiently, they can offer highly liquid secondary claims (like demand deposits) to savers while holding relatively illiquid primary assets, which would carry high transaction costs for an individual to sell quickly.

In summary, the book characterizes transaction cost economies as a vital function that allows FIs to stand between households and corporations, making the transfer of funds more efficient and less expensive for the average saver.

Maturity Intermediation

Maturity intermediation is one of the “special” core functions performed by financial institutions (FIs) that provides significant economic benefits by bridging the gap between the mismatched timing needs of savers and borrowers.

Mechanism of Maturity Intermediation

This function arises from an FI’s ability to better bear the risk of mismatching the maturities of its assets and liabilities than individual household savers can. By engaging in maturity mismatching, FIs provide a vital service to both sides of the economy:

- For Borrowers: FIs can produce long-term contracts, such as 30-year fixed-rate mortgages, which are essential for sectors like residential real estate.

- For Savers: FIs raise funds for these long-term investments through short-term liability contracts, such as demand deposits, which allow savers to maintain liquidity for near-term consumption.

Economic Benefits and Social Welfare

Within the larger context of economic benefits, maturity intermediation contributes to a net social welfare benefit in several ways:

- Overcoming Market Imperfections: In a world without FIs, the long-term nature of corporate debt and equity would create a disincentive for households to invest, as they might prefer holding cash for liquidity reasons. Maturity intermediation removes this friction.

- Encouraging Higher Savings: By offering liquid, short-term claims to savers while financing long-term projects, FIs encourage a higher overall rate of savings in the economy than would otherwise exist.

- Targeted Credit Allocation: This function allows FIs to be the primary source of financing for critical sectors—specifically farming and residential real estate—that have been identified by policymakers as being in special need of support.

Managing the Associated Risks

While maturity mismatching is a core benefit, it inherently exposes FIs to interest rate risk. However, the book highlights that large FIs are uniquely equipped to manage this risk in ways individuals cannot:

- Diversification: Large FIs can use risk diversification and the law of large numbers to predict expected returns more accurately, allowing them to fulfill promises of liquidity on short-term liabilities despite holding long-term assets.

- Superior Market Access: FIs have access to sophisticated hedging markets and instruments that individual savers do not, including loan sales, securitization, futures, swaps, options, caps, and floors.

In summary, maturity intermediation is a fundamental component of FI “specialness” because it transforms the illiquid, long-term credit needs of the economy into the liquid, short-term savings products desired by households, thereby facilitating economic growth and stability.

Denomination Intermediation

Denomination intermediation is a specialized service provided by certain financial institutions (FIs)—most notably mutual funds—that allows small investors to overcome barriers to entry in high-value financial markets. This function is a critical component of the broader economic benefits FIs provide by addressing market imperfections that would otherwise discourage individual savings.

The book highlights several key aspects of denomination intermediation within the context of these economic benefits:

Overcoming Market Entry Barriers

Many attractive financial assets are issued in “very large denominations” that are practically out of reach for the average household saver. For example:

- Negotiable Certificates of Deposit (CDs): These typically have a minimum size of $100,000.

- Commercial Paper: Short-term corporate debt is often sold in minimum packages of $250,000 or more.

Without FIs to act as intermediaries, an individual saver would either be completely excluded from these markets or be forced to hold a “highly undiversified asset portfolio” just to meet the minimum purchase requirements.

The Mechanism of Pooling

FIs perform denomination intermediation by pooling the resources of many small savers. By grouping these small sums together, the FI can purchase large-denomination instruments in bulk. This process transforms large, individual claims into smaller, more accessible “secondary” securities (such as mutual fund shares) that represent a fractional interest in the larger pool.

Broader Economic and Social Benefits

In the larger context of why FIs are special, denomination intermediation provides significant social and economic advantages:

- Increased Access to Higher Returns: Indirect access to wholesale markets allows small savers to “generate higher returns on their portfolios” than they might achieve through traditional, smaller-scale investment options.

- Enhanced Diversification: Because FIs pool funds to buy many different large-denomination assets, they allow small investors to enjoy the risk-reduction benefits of diversification that would be impossible to achieve individually.

- Increased Rate of Savings: By removing the “imperfections” and constraints imposed by large minimum denominations, FIs make investing more accessible and attractive. This ultimately “encourages a higher rate of savings than would otherwise exist” in the economy, providing more capital for corporate users of funds.

The importance of this function is reflected in recent industry trends: the book notes a dramatic rise in the market share of investment companies (mutual funds), largely because savers increasingly prefer the denomination intermediation and information services they provide over the traditional transformed claims offered by banks and insurance companies.

Social Services

In the larger context of why financial institutions (FIs) are considered “special,” the book describes social services (also referred to as social welfare benefits) as essential functions that benefit the economy as a whole, rather than just individual savers or borrowers. These services go beyond simple market intermediation and are a primary reason why FIs are subject to extensive government regulation.

The source material identifies five specific areas of social service that contribute to the “specialness” of FIs:

1. Transmission of Monetary Policy

Depository institutions serve as the vital conduit through which the Federal Reserve’s monetary policy actions—such as setting interest rates or reserve requirements—impact the rest of the financial system and the general economy. Because their deposit liabilities form the core of the money supply, DIs are essential for controlling inflation and economic growth.

2. Credit Allocation

FIs are often the major, and sometimes the only, source of financing for critical sectors of the economy that are pre-identified as being in special need of support, such as farming and residential real estate. By providing credit to make farms viable or houses more affordable, FIs contribute to a more stable and productive society.

3. Intergenerational Wealth Transfers (Time Intermediation)

FIs, specifically life insurance companies and pension funds, provide the social benefit of allowing savers to transfer wealth across generations. This function is often supported by the government through special tax treatments and subsidies to ensure the social well-being of a country’s population.

4. Efficient Payment Services

The provision of efficient check-clearing and wire transfer services (such as Fedwire and CHIPS) directly benefits the economy. These systems are so integrated into daily economic life that a breakdown in their operation could produce gridlock in the payment system and cause widespread harm.

5. Denomination Intermediation

FIs like mutual funds allow small investors to overcome constraints imposed by the large minimum denominations of certain assets (e.g., $250,000 commercial paper). By pooling small sums of money, FIs give household savers indirect access to these markets, which encourages a higher rate of savings and allows small savers to generate higher returns.

The Link to Regulation and Negative Externalities

The book emphasizes that these social services are so critical that a failure to provide them efficiently imposes negative externalities on the entire community. For example, a bank failure not only destroys individual savings but also restricts a firm’s access to credit and may cause a “contagious” loss of confidence in the entire financial system. This unique social role justifies the net regulatory burden—the private cost of adhering to safety, soundness, and consumer protection regulations—as a necessary trade-off for maintaining a smooth and stable economy.

Monetary Policy Transmission

In the context of why financial institutions (FIs) are considered special, the transmission of monetary policy is identified as a vital social service (or social welfare benefit) that benefits the overall economy. While other FI functions focus on individual savers or borrowers, social services are essential for the smooth operation and stability of the entire financial system.

The Role of Depository Institutions as a Conduit

Depository institutions (DIs) are uniquely “special” in this regard because they serve as the primary conduit through which the Federal Reserve’s monetary policy actions impact the rest of the financial system and the economy. This special role exists because:

- Money Supply Foundation: The highly liquid deposit contracts issued by DIs form the core of the most commonly used definitions of the money supply, such as M1 and M2.

- Control of Inflation and Growth: Because these liabilities are a significant component of the money supply, they directly impact the rate of inflation and economic growth.

- Implementation of Policy: When the central bank takes actions—such as conducting open market operations, setting the discount rate, or establishing reserve requirements—it relies on the banking system to transmit these changes to the broader economy.

The Link to Social Welfare and Regulation

This function is classified as a social service because its efficient provision is critical to a country’s economic health. A breakdown in this transmission—such as during a bank failure or a systemic financial crisis—can impose negative externalities on the entire community, including the destruction of household savings and the restriction of credit to firms.

Because of this vital social impact, FIs are subject to monetary policy regulation. Regulators often impose formal controls, such as minimum cash reserve requirements, to make the transmission of monetary policy more predictable. While these regulations may impose a net regulatory burden on the private institution (acting as a “tax” on their operations), they are intended to protect the social welfare benefits of a stable monetary system.

Historical Significance

The importance of this social service was highlighted during the financial crisis of the late 2000s. Governments and central banks across the world bailed out numerous depository institutions specifically so they could continue to implement aggressive monetary policy actions to combat collapsing financial markets. This underscores that the transmission function is not just a business activity, but a critical social service that justifies extraordinary government support and oversight.

Credit Allocation

In the context of why financial institutions (FIs) are considered special, the book identifies credit allocation as a vital social service (or social welfare benefit) provided to the economy. While many FI functions provide individual benefits to savers and borrowers, these social services provide broader benefits to society as a whole.

The Role of FIs in Targeted Financing

Credit allocation is viewed as a special service because FIs are often the major, and sometimes the only, source of financing for particular sectors of the economy that have been pre-identified by policymakers as being in special need of support.

- Key Sectors: The book specifically highlights farming and residential real estate as critical areas that rely on this credit allocation.

- Societal Impact: The fundamental logic behind this social service is that providing credit to make farms more viable or houses more affordable leads to a more stable and productive society.

Institutional Specialization and Support

Certain types of FIs are considered “more special” because they have traditionally served these specific sectors:

- Residential Real Estate: In the United States, savings associations and savings banks have historically functioned as the primary lenders for this sector.

- Farming: The U.S. government has directly encouraged specialized financing for agriculture through the creation of Federal Farm Credit Banks.

Link to Credit Allocation Regulation

Because these sectors are deemed socially important, they are supported by specific credit allocation regulations. These regulations ensure that FIs continue to direct funds toward these areas:

- Requirements and Restrictions: These laws may require an FI to hold a minimum amount of assets in a particular sector or may set maximum interest rates and fees to subsidize certain types of loans.

- The QTL Test: A primary example is the qualified thrift lender (QTL) test, which requires savings institutions to maintain at least 65 percent of their assets in residential mortgage-related assets to retain their thrift charter.

- Net Regulatory Burden: While these regulations provide social welfare benefits, they also impose private costs on FIs, such as the expense of meeting asset restrictions or the loss of income from interest rate caps. These costs contribute to the net regulatory burden—the difference between the private costs of regulation and the private benefits, such as deposit insurance, that an FI receives.

Wealth Transfers

In the context of why financial institutions (FIs) are considered special, the book identifies intergenerational wealth transfers (also referred to as time intermediation) as a vital social service or social welfare benefit. This function is primarily fulfilled by life insurance companies and pension funds, which provide savers with the essential ability to transfer wealth from one generation to the next.

The book highlights several key aspects of this social service:

- Societal Importance: The ability of citizens to transfer wealth across generations is of “great importance to the social well-being of a country”. It allows individuals to protect themselves and their beneficiaries against major life risks, such as future ill health or falling income upon retirement.

- Government Support and Subsidies: Because of its social significance, this wealth transfer process is often actively encouraged by the government. This support typically comes in the form of special taxation relief and other subsidy mechanisms, which allow these transfers to avoid the full marginal tax treatment that a direct payment between individuals might otherwise incur.

- Role of Specific Institutions: While all FIs channel funds, life insurance companies and pension funds are specifically recognized as the best-suited intermediaries for this function. They act as specialists in managing long-term savings and provide the contractual frameworks (like whole life insurance or annuities) necessary to facilitate these multi-generational transfers.

- Link to Regulation: This social service is so critical to the general economy and society that a breakdown in its efficient provision—such as an insurance company failure—could leave households “totally exposed in old age to catastrophic illnesses”. This unique role in safeguarding long-term social welfare is a primary justification for the safety and soundness regulation imposed on these institutions.

In summary, the book characterizes wealth transfers not just as a financial product, but as a fundamental social service that benefits the country’s overall social well-being, justifying both government tax subsidies and extensive regulatory oversight.

Payment Services

In the larger context of why financial institutions (FIs) are considered special, the provision of payment services is identified as a vital social service (or social welfare benefit) that directly benefits the overall economy. While some FI functions focus on individual risk transformation, these social services are essential for maintaining a stable and efficient economic environment.

The book highlights several key aspects of payment services within this framework:

- Primary Providers: Depository institutions are recognized as the special providers of these services. Their efficiency in managing these systems is a core component of their “specialness” in the financial system.

- Key Service Types: The two most important payment services provided are check-clearing and wire transfer services.

- Wholesale Networks: The book specifically mentions Fedwire and CHIPS as the two large wholesale payment wire networks in the United States. These systems facilitate the transfer of trillions of dollars daily.

- Economic Impact and Efficiency: The efficiency of these payment systems is critical; any breakdown in their operation would likely produce gridlock in the payment system, resulting in widespread and harmful effects on the entire economy.

- Link to Regulation and Negative Externalities: Because payment services are so integrated into daily economic life, a failure in their provision would impose significant negative externalities on both the ultimate sources(households) and users (firms) of savings. This systemic importance justifies the extensive safety and soundness regulation that depository institutions face to prevent disruptions that could cripple financial markets.

In summary, the book characterizes payment services not merely as a business line for banks, but as a fundamental social service that ensures the smooth flow of funds across the economy, necessitating government oversight to protect against systemic shocks.

— Linden Lake

This Series

→ Book Review (4 of 4): Financial Institutions Management – A Risk Management Approach — Industry Trends and Risk

→ Book Review (3 of 4): Financial Institutions Management – A Risk Management Approach — Regulation and Oversight

→ Book Review (2 of 4): Financial Institutions Management – A Risk Management Approach — Types of Depository Institutions

→ Book Review (1 of 4): Financial Institutions Management – A Risk Management Approach — Why Financial Institutions Are Special

Leave a Reply