While exploring recent developments in the application of data science and emerging technologies in accounting, I repeatedly encountered the concept of Triple-Entry Accounting (TEA). Although the idea has existed for some time, advances in blockchain technology have renewed interest in its potential to reshape financial recordkeeping and auditing.

One article that provides a concise introduction to the concept is published in the Journal of Risk and Financial Management and can be found here:

https://www.mdpi.com/1911-8074/18/9/525

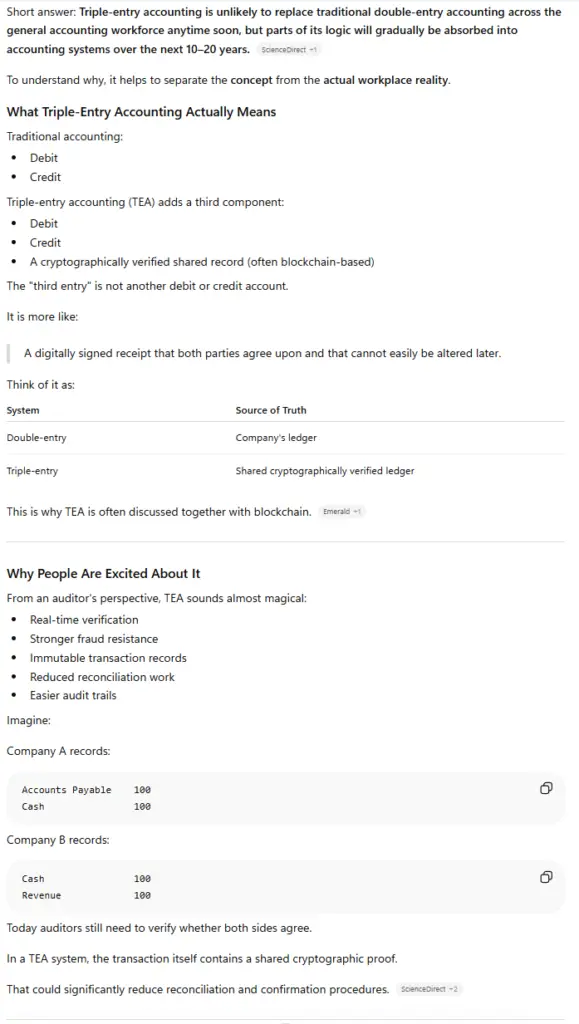

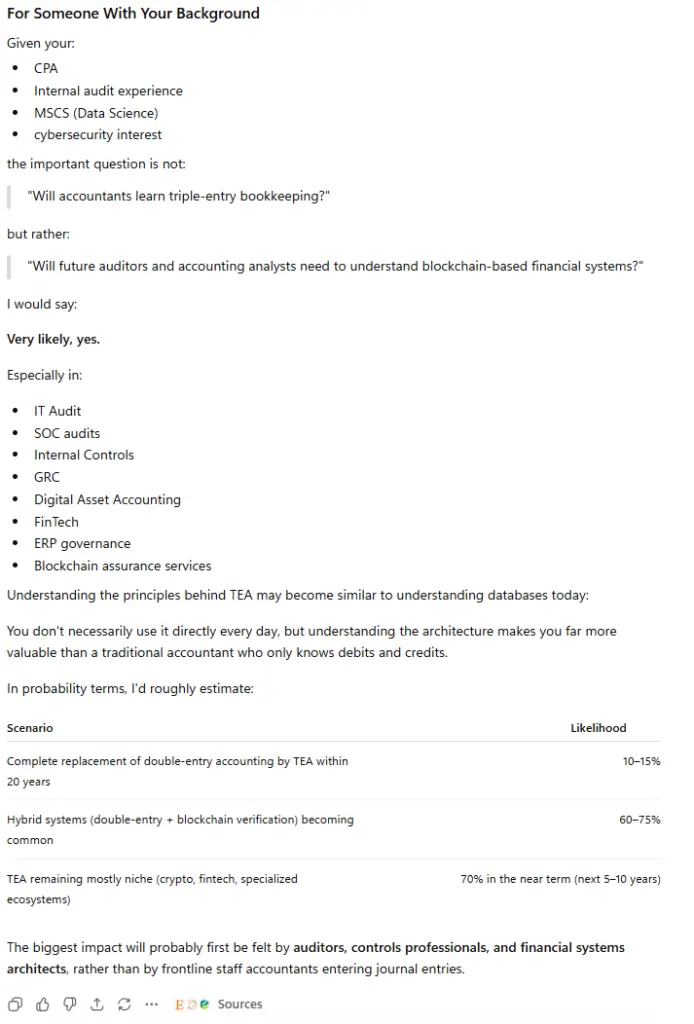

Curious about its practical implications, I asked ChatGPT how likely Triple-Entry Accounting is to be adopted in the workplace over the coming decades. One part of the response particularly caught my attention. It estimated that the probability of Triple-Entry Accounting completely replacing traditional double-entry accounting within the next 10–20 years may be relatively low—perhaps in the range of 10–15%. Instead, it suggested that TEA is more likely to remain concentrated in specialized areas such as cryptocurrency, fintech, and blockchain-native ecosystems.

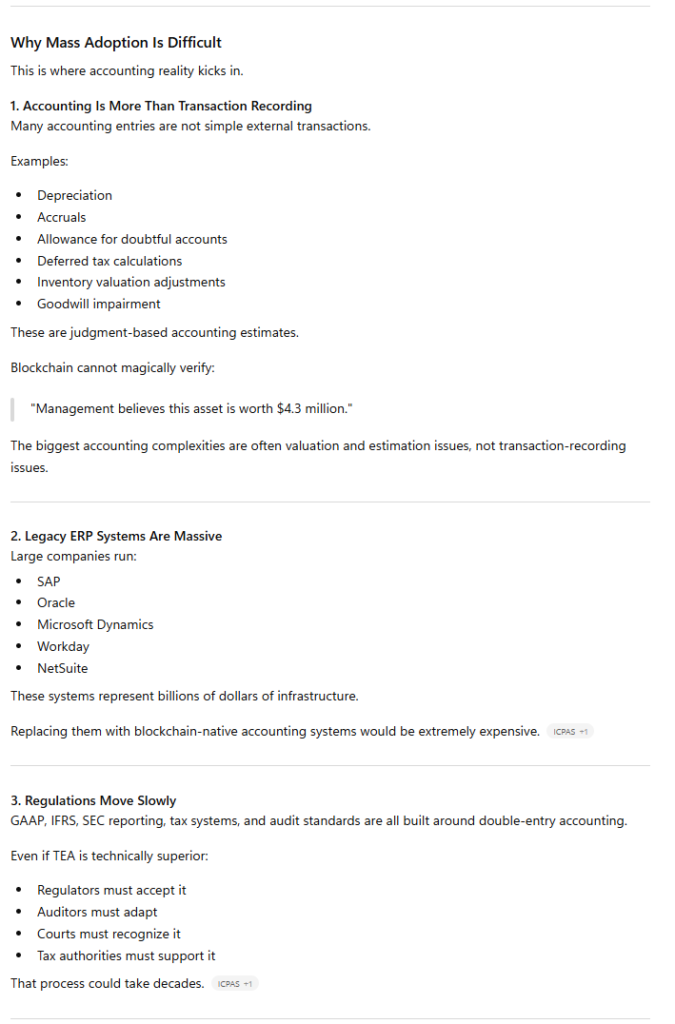

This assessment seems reasonable. Accounting is not merely a system for recording transactions; it also involves estimates, judgments, valuations, and regulatory compliance. Many of these functions cannot be fully solved by cryptographic verification alone.

That said, one factor worth considering is the future development of quantum computing. Some researchers believe commercially viable quantum systems may emerge between the late 2020s and mid-2030s. If sufficiently powerful quantum computers become a reality, many of today’s cryptographic methods—including those underlying certain blockchain architectures—could face significant challenges. While researchers are already developing post-quantum cryptographic standards, the long-term relationship between blockchain technology and accounting remains an open question.

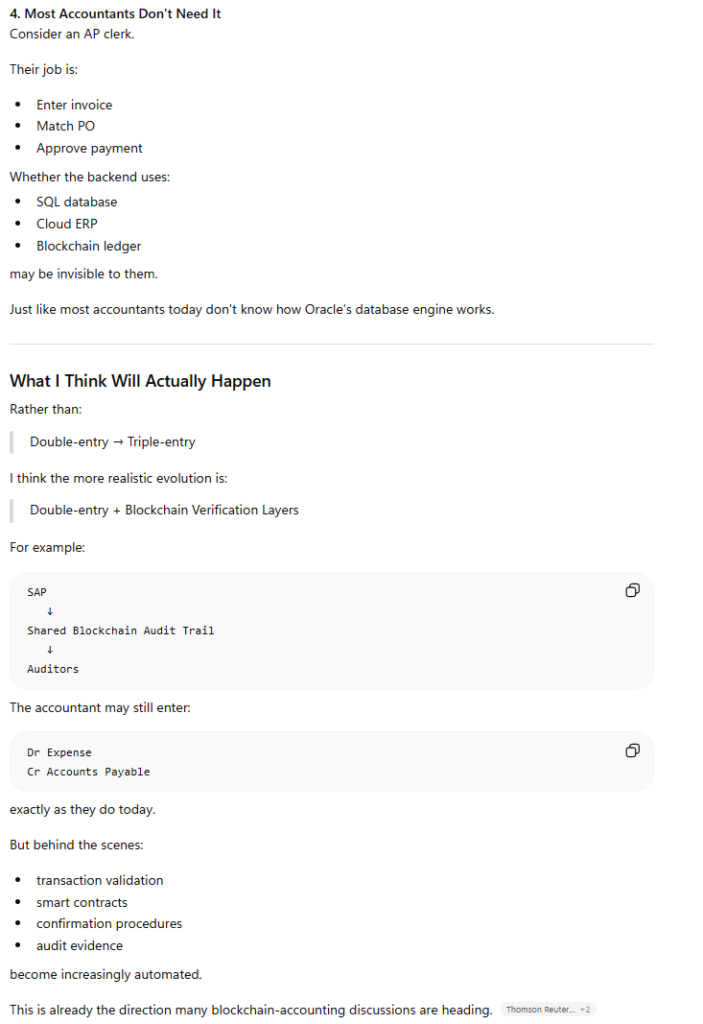

For now, Triple-Entry Accounting appears less likely to replace double-entry accounting than to complement it. Its greatest contribution may not be a new bookkeeping method, but rather a new layer of trust, verification, and transparency within increasingly digital financial systems.

— Linden Lake

Leave a Reply