In the book, money is defined as anything that is generally accepted as payment for goods or services or in the repayment of debts. It is a central theme because of its profound impact on economic variables such as inflation, business cycles, and interest rates. Understanding money requires distinguishing it from related concepts: while “the book” notes that people often use the term synonymously with wealth or income, economists view wealth as the total collection of property that stores value and income as a flow of earnings per unit of time.

The Primary Functions of Money

The book identifies three essential functions that money performs in an economy:

- Medium of Exchange: Money is used to pay for goods and services, promoting economic efficiency by eliminating the “double coincidence of wants” required in a barter economy. This lubricant lowers transaction costs and allows individuals to specialize in what they do best.

- Unit of Account: Money provides a standardized measure of value. Without it, a complex economy with 1,000 goods would require nearly 500,000 different prices to facilitate trade; money reduces this to only 1,000 prices, dramatically lowering the time spent comparing values.

- Store of Value: Money acts as a repository of purchasing power over time. While it is the most liquid asset—meaning it can be converted into a medium of exchange quickly and without loss of value—its effectiveness as a store of value is diminished during periods of high inflation.

The Evolution of the Payments System

The book traces how the form of money has changed as the payments system evolved to reduce the costs of conducting transactions.

- Commodity Money: Early money consisted of valuable commodities like precious metals, which were often heavy and difficult to transport.

- Fiat Money: Paper currency eventually evolved into fiat money, which is decreed by governments as legal tender but is not convertible into precious metals.

- Checks and Electronic Payment: The introduction of checks further reduced transportation costs and improved efficiency. Today, the system is moving toward electronic money (e-money), including debit cards, stored-value cards, and e-cash.

- Cryptocurrency: The book specifically analyzes Bitcoin, concluding that while it serves as a medium of exchange, it currently fails to function effectively as a unit of account or a store of value due to its extreme price volatility.

Measuring Money: M1 and M2

Because various assets can function as money, the Federal Reserve uses “monetary aggregates” to measure the money supply.

- M1: This is the narrowest measure, consisting of the most liquid assets: currency, traveler’s checks, demand deposits, and other checkable deposits.

- M2: This broader measure includes all of M1 plus “near moneys” that are not quite as liquid but can be converted into cash quickly, such as savings deposits, small-denomination time deposits, and money market mutual fund shares.

The Larger Economic Context

The book emphasizes that the growth rate of the money supply is a critical determinant of long-run inflation. Citing Milton Friedman’s famous adage that “inflation is always and everywhere a monetary phenomenon,” the book provides data showing that countries with the highest money growth rates also tend to have the highest inflation rates. Furthermore, changes in money growth often precede economic recessions, suggesting a strong link between the money supply and the health of the broader financial system. This makes the precise measurement of money essential for policymakers, particularly when M1 and M2 growth rates diverge and send conflicting signals about the stance of monetary policy.

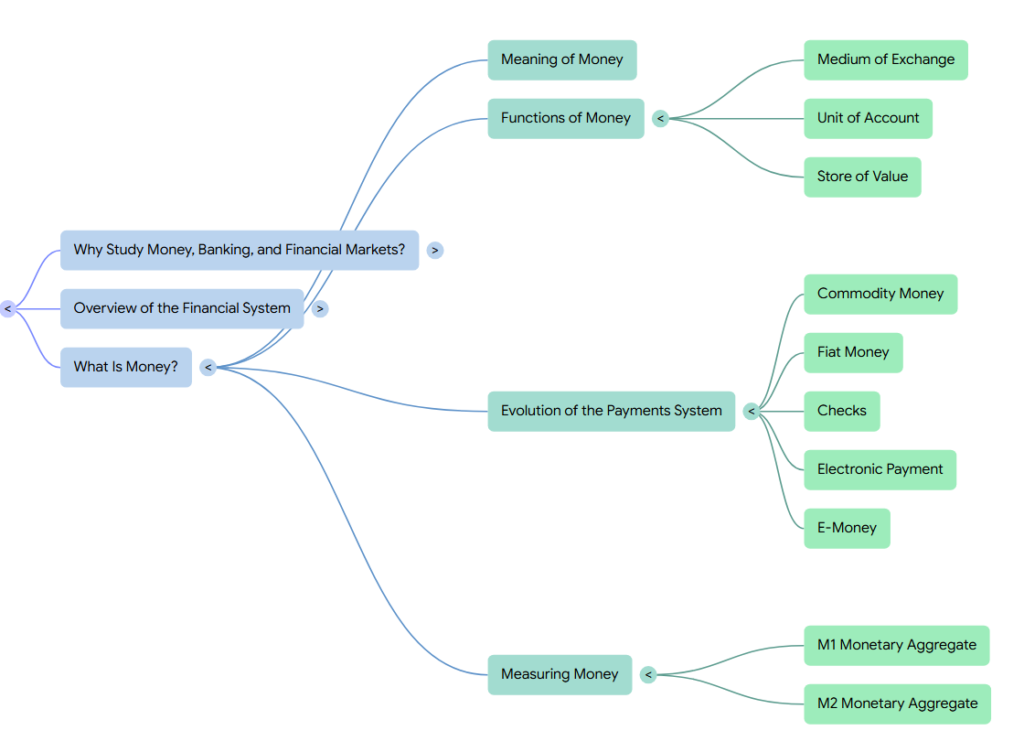

Meaning of Money

In the book, money is defined with a specific technical meaning that differs from its common usage in everyday conversation. Economists define money (also referred to as the money supply) as anything that is generally accepted as payment for goods or services or in the repayment of debts.

Distinguishing Money from Related Concepts

To provide a precise meaning, the book distinguishes money from several other terms with which it is frequently confused:

- Money vs. Currency: While many people use “money” to mean only currency (paper bills and coins), the book argues this definition is too narrow. Because checks are also accepted for payment, checking account deposits are considered money as well.

- Money vs. Wealth: People often use money synonymously with wealth (e.g., “Joe has an awful lot of money”). The book clarifies that wealth is the total collection of pieces of property that serve to store value, including not only money but other assets like bonds, stocks, art, land, and cars.

- Money vs. Income: The book distinguishes between money, which is a stock (a certain amount at a given point in time), and income, which is a flow of earnings per unit of time. For example, telling someone you have $1,000 in your pocket (money) is an exact measure, whereas saying you have an income of $1,000 requires a time frame (per month, per year) to be meaningful.

The Context of “What Is Money?”

The “Meaning of Money” section serves as the foundational definition for the broader discussion in the chapter regarding why money is essential to the economy. This definition allows the book to explore:

- The Functions of Money: Money is unique because of its primary function as a medium of exchange, which distinguishes it from other assets that may serve as stores of value but cannot be used easily to pay for goods. It also serves as a unit of account and a store of value.

- The Evolution of Payments: Because money is defined by people’s behavior—specifically, what they are willing to accept as payment—its form has evolved from commodity money (like gold) to fiat money, checks, and electronic money.

- Measuring Money: Because the behavioral definition of money is broad, the book notes that the Federal Reserve must create specific “monetary aggregates” (like M1 and M2) to provide precise, measurable definitions for the purpose of conducting monetary policy.

Functions of Money

In the book, money is defined by its functions rather than its form; whether it consists of shells, gold, or paper, it is identified as anything that performs three primary roles: a medium of exchange, a unit of account, and a store of value. Within the larger context of “What Is Money?”, these functions explain why money is essential for an efficient, well-functioning economy.

1. Medium of Exchange

The most distinctive function of money is its use as a medium of exchange to pay for goods and services.

- Promoting Efficiency: The book explains that money increases economic efficiency by minimizing the time spent exchanging goods—known as transaction costs.

- Eliminating Barter Hurdles: In a barter economy, trade requires a “double coincidence of wants,” where two parties must each happen to have exactly what the other desires. Money acts as a lubricant that eliminates this requirement, allowing individuals to specialize in what they do best and then use their earnings to buy what they need.

- Requirements for Effectiveness: For a commodity to function effectively in this role, it must be easily standardized, widely accepted, divisible, easy to carry, and durable.

2. Unit of Account

Money serves as a unit of account, providing a standardized measure of value in the economy.

- Reducing Price Complexity: Without a unit of account, a barter economy with 1,000 different goods would require nearly 500,000 different exchange rates (prices) to facilitate trade between every possible pair of items. By quoting all prices in terms of a single unit (like dollars), the number of prices that must be considered is reduced to only 1,000.

- Lowering Transaction Costs: By simplifying the comparison of values, this function further lowers the time and effort spent in the marketplace.

3. Store of Value

Money also functions as a store of value, acting as a repository of purchasing power that can be saved and spent at a later date.

- Liquidity: While other assets (like stocks, bonds, or real estate) can store wealth and may offer higher returns, money is unique because it is the most liquid asset. Liquidity refers to the relative ease and speed with which an asset can be converted into a medium of exchange. Because money is the medium of exchange, it does not have to be converted to make purchases.

- Impact of Price Levels: The effectiveness of money as a store of value is highly dependent on the price level. During periods of hyperinflation (where inflation exceeds 50% per month), money loses value so rapidly that it performs this role poorly, often leading people to abandon it in favor of barter systems.

Context within “What Is Money?”

The book emphasizes that these three functions are what give money its technical meaning in economics, distinguishing it from “currency” (which is too narrow) or “wealth” (which is too broad) . While many items can function as a store of value, only something that is generally accepted as a medium of exchange is considered “money” in the eyes of an economist.

Medium of Exchange

In the book, the function of money as a medium of exchange is identified as its most distinctive role, serving as the primary feature that distinguishes money from other assets like stocks, bonds, or real estate. It is defined as anything used to pay for goods and services.

Promoting Economic Efficiency

The book explains that money as a medium of exchange is essential for a well-functioning economy because it dramatically increases economic efficiency. It achieves this by:

- Minimizing Transaction Costs: In a barter economy—where goods and services are traded directly for other goods—the “transaction cost,” or the time and effort spent trying to exchange items, is extremely high.

- Eliminating the Double Coincidence of Wants: For a trade to occur in a barter system, two parties must each possess exactly what the other desires, a requirement known as the “double coincidence of wants”. Money acts as a lubricant that removes this hurdle, allowing individuals to trade their labor or products for money and then use that money to buy what they need from others.

- Encouraging Specialization: By lowering transaction costs and making trade easier, money allows people to specialize in what they do best, facilitating a more productive division of labor in society.

Criteria for an Effective Medium of Exchange

According to the book, for a commodity to function effectively in this role, it must satisfy five specific criteria:

- Standardization: Its value must be easy to ascertain.

- Wide Acceptance: It must be universally desired or accepted as payment.

- Divisibility: It must be easy to “make change” for transactions of different sizes.

- Portability: It must be easy to carry.

- Durability: It must not deteriorate or rot quickly.

The book notes that many diverse objects have fulfilled these criteria throughout history, including wampum (beads), tobacco, whiskey, and even cigarettes in prisoner-of-war camps.

Context within the Functions of Money

While money also serves as a unit of account (measuring value) and a store of value (saving purchasing power), the medium of exchange function is the most fundamental. The book highlights that while many assets can serve as a store of value, their lack of liquidity—the ease with which they can be converted into a medium of exchange—makes them less efficient than money for conducting daily transactions. Furthermore, during periods of extreme inflation, the medium of exchange function can break down; the book cites instances of hyperinflation where money lost its value so rapidly that people abandoned it in favor of barter, causing transaction costs to skyrocket and economic output to fall.

Unit of Account

In the book, the unit of account is defined as the function of money used to measure value in an economy. Along with serving as a medium of exchange and a store of value, it is one of the three primary functions that give money its technical meaning in economics.

Solving the Barter Price Problem

The book explains that the importance of the unit of account is best understood by looking at a barter economy, which lacks a standardized measure of value. Without a single unit of account, the price of every good must be quoted in terms of every other good.

- Price Complexity: In an economy with only three goods, you would need to know three different prices (e.g., peaches in terms of movies, movies in terms of lectures, etc.).

- The Price Formula: As the number of goods () increases, the number of required prices grows exponentially according to the formula .

- Numerical Examples: Following this formula, an economy with 10 goods would require 45 different prices; an economy with 100 goods would require 4,950 prices; and a supermarket with 1,000 different goods would require a staggering 499,500 different prices.

Reducing Transaction Costs

The book identifies the unit of account as a vital tool for reducing transaction costs. By quoting all prices in terms of a single unit (such as dollars), the number of prices a consumer needs to consider in a 1,000-good economy is reduced from nearly 500,000 to just 1,000. This allows individuals to compare the relative value of different goods and services with far less time and effort.

Significance within the Functions of Money

While the medium of exchange is the function that most clearly distinguishes money from other assets like stocks or bonds, the unit of account is essential for the economy to run smoothly as it becomes more complex. The book notes that the benefits of this function grow as an economy expands and more goods and services are traded. However, its effectiveness can be compromised; in the book’s discussion of Bitcoin, it notes that the cryptocurrency currently fails to function effectively as a unit of account because its extreme price volatility makes it difficult to use as a reliable measure of value.

Store of Value

In the book, a store of value is defined as a repository of purchasing power that is available over time. Along with serving as a medium of exchange and a unit of account, it is one of the three primary functions that give money its technical meaning in economics.

Saving Purchasing Power

The book explains that the store-of-value function is useful because most people do not want to spend their income immediately upon receiving it; instead, they prefer to wait until they have the time or desire to shop. This function allows individuals to save purchasing power from the time income is received until the time it is spent.

Liquidity and Comparison to Other Assets

While many other assets—such as stocks, bonds, land, houses, or jewelry—can also function as a store of value, the book notes that money possesses a unique advantage: liquidity.

- Definition of Liquidity: This refers to the relative ease and speed with which an asset can be converted into a medium of exchange.

- The Advantage of Money: Money is the most liquid asset of all because it is the medium of exchange; unlike other assets, it does not have to be converted into anything else to make purchases.

- Drawbacks of Money: Despite its liquidity, money is often a less attractive store of value than other assets because it usually pays a lower interest rate and does not experience price appreciation.

Impact of the Price Level and Inflation

The effectiveness of money as a store of value is highly dependent on the aggregate price level. The book explains that a doubling of all prices means the value of money has dropped by half.

- Inflation: When the price level increases rapidly, money loses its value quickly, and people become more reluctant to hold their wealth in this form.

- Hyperinflation: During periods of extreme inflation (exceeding 50% per month), money performs this role so poorly that its use to carry out transactions declines, and the economy may return to a barter system.

The book concludes that while money is the most liquid asset, its quality as a store of value is compromised during inflationary periods, which can lead to increased transaction costs and a sharp fall in economic output.

Evolution of the Payments System

In the book, money is defined by people’s behavior as anything generally accepted as payment for goods or services or in the repayment of debts. The evolution of the payments system—the method of conducting transactions in an economy—reflects a centuries-long effort to reduce the costs of conducting these transactions and improve economic efficiency.

The Stages of Evolution

The book traces the transformation of money through several distinct forms:

- Commodity Money: For most of human history, money consisted of valuable commodities like precious metals (gold or silver). While universally acceptable, commodity money was difficult to transport and heavy, making large transactions cumbersome.

- Fiat Money: The next major development was paper currency, which evolved into fiat money—paper currency decreed as legal tender by governments but not convertible into precious metals. Fiat money is much lighter than metal, but its success depends on public trust in the issuing authorities and the technical ability to prevent counterfeiting.

- Checks: A check is an instruction from a depositor to a bank to transfer funds to another account. Checks improved efficiency by allowing large transactions to occur without moving actual currency and by providing convenient receipts. However, the book notes that checks have drawbacks, including the time required for delivery and the high “paper shuffling” costs associated with processing them.

- Electronic Payment: The spread of the Internet and inexpensive computers has made it cost-effective to pay bills electronically, offering significant savings over mailing paper checks.

- Electronic Money (E-Money): This is money that exists only in electronic form. Key forms include:

- Debit Cards: These allow for the immediate electronic transfer of funds from a consumer’s bank account to a merchant.

- Stored-Value and Smart Cards: These range from simple prepaid cards to sophisticated “smart cards” containing computer chips that can be loaded with digital cash.

- E-Cash: Used specifically for purchasing goods and services over the Internet.

Modern and Future Developments

The book analyzes Bitcoin as a decentralized type of electronic money created in 2009. While it functions as a medium of exchange, the book concludes that its extreme volatility currently prevents it from serving effectively as a unit of account or a store of value.

Despite the efficiency of electronic payments, the book notes that the transition to a cashless society has been slow due to several obstacles. These include the high cost of setting up the necessary telecommunications networks, security concerns regarding hackers, and privacy worries related to the electronic trail of personal data created by digital transactions. Consequently, the book suggests that reports of the total disappearance of cash are “greatly exaggerated”.

Commodity Money

In the book, the evolution of the payments system is described as a centuries-long process of developing new methods for conducting transactions to reduce costs and improve economic efficiency. Commodity money represents a foundational stage in this evolution, serving as the primary medium of exchange from ancient times until several hundred years ago in almost all but the most primitive societies.

Definition and Function

Commodity money is defined as money made up of precious metals or another valuable commodity. The book notes that for any object to function as money, it must be universally acceptable; therefore, items that clearly have value to everyone were the natural choice for early payments systems.

Criteria and Historical Examples

For a commodity to function effectively as money, the book specifies that it must meet five key criteria:

- Standardization: Its value must be easily ascertained.

- Wide Acceptance: It must be universally desired or accepted.

- Divisibility: It must be easy to “make change” for different-sized transactions.

- Portability: It must be easy to carry.

- Durability: It must not deteriorate or rot quickly.

Historical examples of commodity money mentioned in the book include wampum (strings of beads) used by Native Americans, tobacco and whiskey used by early American colonists, and even cigarettes used in prisoner-of-war camps during World War II. Precious metals like gold and silver were the most common forms used for much of human history.

The Role in Systemic Evolution

In the larger context of the payments system, commodity money eventually proved too cumbersome for an expanding economy. The book highlights that the primary problem with a system based exclusively on precious metals was that they were very heavy and hard to transport. For example, a large purchase like a house would have required a truck to transport the necessary amount of metal coins.

These physical limitations spurred the next major developments in the evolution of the payments system:

- Paper Currency: Initially, this was a lighter alternative that carried a guarantee of being convertible into coins or a fixed quantity of precious metal.

- Fiat Money: Currency eventually evolved into fiat money, which is decreed as legal tender by governments but is no longer convertible into precious metals.

- Checks and Electronic Payments: These subsequent innovations further reduced the need to transport physical money, continuing the evolutionary trend of lowering transaction costs.

Fiat Money

In the book, fiat money represents a critical stage in the evolution of the payments system, developing as a more efficient successor to commodity money. It is defined as paper currency that is decreed by a government as legal tender—meaning it must be accepted as legal payment for debts—but is not convertible into coins or precious metals.

Role in the Payments System Evolution

The transition to fiat money solved a significant problem inherent in a system based on precious metals: weight. While commodity money was heavy and cumbersome to transport for large transactions, fiat money provided the advantage of being much lighter and easier to carry. Because this form of money has evolved into a legal arrangement rather than a physical commodity, the book notes that countries have the flexibility to change their currency at will, such as when many European nations abandoned their domestic currencies for the euro in 2002.

Requirements for Acceptance

The book emphasizes that fiat money cannot function as a medium of exchange based on its intrinsic value; rather, its acceptance depends on two key factors:

- Public Trust: People must have faith in the authorities that issue the currency.

- Anti-Counterfeiting Measures: Printing technology must be sufficiently advanced so that counterfeiting the currency is extremely difficult.

Limitations and Further Evolution

Despite its advantages in portability, the book identifies major drawbacks to fiat money that spurred further innovations in the payments system. Specifically, paper currency and coins are easily stolen and can still be expensive to transport in very large amounts because of their bulk. These limitations eventually led to the development of modern banking and the invention of checks, which allowed for the transfer of funds without the physical movement of currency.

Checks

In the book, the invention of checks is described as a major innovation in the evolution of the payments system, arising alongside the development of modern banking to improve economic efficiency. A check is defined as an instruction from a depositor to their bank to transfer money from their account to another person’s account upon deposit.

Role in the Evolution of Payments

The book places checks as a critical evolutionary step following the development of fiat money . While paper currency was a significant improvement over heavy commodity money (like gold), it remained easily stolen and expensive to transport in large quantities. Checks solved these issues by allowing for the transfer of funds without the physical movement of currency.

Advantages of a Check-Based System

The book identifies several key benefits that checks brought to the payments system:

- Reduced Transportation Costs: Large transactions became much easier because checks can be written for any amount up to the account balance, eliminating the need to move physical cash.

- Improved Efficiency: Payments made back and forth between parties can often be settled by simply canceling the checks, further reducing the need for currency movement .

- Increased Safety: Because they replace large amounts of cash, the risk of loss from theft is greatly reduced.

- Record Keeping: Checks provide convenient, permanent receipts for purchases.

Drawbacks and Limitations

Despite these improvements, the book notes that a payments system based on checks has two significant problems that eventually spurred the move toward electronic payments:

- Processing Time: It takes time for checks to travel from one location to another, and banks often wait several business days before allowing a depositor to use the funds from a deposited check. This delay can be frustrating for those with urgent cash needs.

- High Costs: The “paper shuffling” required to process checks is extremely expensive; the book estimates that the cost of processing all checks written in the United States exceeds $10 billion per year.

In the larger context of the payments system’s evolution, these inefficiencies led to the next stages: electronic payments and e-money, which offer even lower transaction costs and faster processing .

Electronic Payment

In the book, the evolution of the payments system is characterized as a long-term process driven by the need to reduce transaction costs and improve the efficiency of the economy. Electronic payment represents a major technological advancement in this sequence, following the development of paper-based checks.

Transition from Paper to Electronic Payments

The book notes that for many years, the primary alternative to physical currency was the check; however, the “paper shuffling” required to process billions of checks annually became increasingly expensive, costing over $10 billion per year in the United States alone. The development of inexpensive computers and the spread of the Internet made it cost-effective to replace these physical instructions with electronic ones. This shift allows individuals to pay bills by logging onto bank websites or by setting up automatic deductions for recurring expenses, which is estimated to save more than one dollar per transaction compared to using paper checks.

Electronic Money (E-Money)

The book distinguishes between electronic payment systems and electronic money (e-money), which is money that exists only in digital form and can substitute for both checks and cash. Several forms of e-money have emerged:

- Debit Cards: These allow for the immediate electronic transfer of funds from a consumer’s bank account to a merchant.

- Stored-Value Cards: These include simple prepaid cards and more sophisticated smart cards, which contain computer chips that can be loaded with digital cash from a bank account.

- E-Cash: This is a form of electronic money used specifically for purchasing goods and services over the Internet.

- Cryptocurrencies: The book analyzes Bitcoin as a newer type of electronic money, though it concludes that its extreme volatility currently prevents it from functioning effectively as a reliable unit of account or store of value.

Obstacles to a Cashless Society

Despite the efficiency and convenience of electronic payments, the book argues that reports of the “death of cash” are exaggerated. Several factors prevent the complete disappearance of paper-based systems:

- Setup Costs: It is extremely expensive to establish the comprehensive telecommunications and card-reader networks required for a purely electronic system.

- Security Concerns: The vulnerability of digital systems to hackers and unauthorized access creates significant fears regarding the safety of electronic funds.

- Privacy Issues: Because electronic transactions leave a digital trail of personal data on buying habits, there are concerns that government agencies or marketers could use this information to encroach on individual privacy.

In the larger context of the evolution of the payments system, while electronic payments have significantly lowered transaction costs, these security and infrastructure hurdles ensure that the transition to a fully checkless and cashless society remains slow.

E-Money

In the book, the evolution of the payments system is described as a centuries-long process aimed at reducing the costs of conducting transactions and improving economic efficiency. Electronic money (e-money) represents the most recent major stage in this evolution, appearing after the development of paper-based checks and electronic payment systems.

Definition and Primary Forms

The book defines e-money as money that exists only in digital form and can substitute for both checks and physical currency. It identifies three primary forms:

- Debit Cards: These allow consumers to purchase goods by electronically transferring funds immediately from their bank accounts to a merchant’s account.

- Stored-Value and Smart Cards: The simplest form is a prepaid card, like a phone card, for a preset dollar amount. A more sophisticated version is the smart card, which contains a computer chip that can be loaded with digital cash from a bank account whenever needed.

- E-Cash: This form of e-money is used specifically on the internet to purchase goods and services.

Bitcoin and the Future of E-Money

The book includes a specific application analyzing Bitcoin, a decentralized type of e-money created in 2009. While Bitcoin functions well as a medium of exchange due to low transaction fees and anonymity, the book concludes it currently fails to satisfy the other two functions of money—acting as a reliable unit of account or store of value—because its price is extremely volatile.

The Context of a “Cashless Society”

Within the larger context of the evolution of payments, e-money provides a path toward a potentially cashless society . However, the book argues that reports of the total disappearance of cash are “greatly exaggerated” due to several significant obstacles:

- Setup Costs: Establishing the telecommunications and card-reader networks necessary for a dominant e-money system is extremely expensive .

- Security Concerns: The vulnerability of digital databases to hackers creates fears regarding the safety of electronic funds .

- Privacy Issues: Because electronic payments leave a digital trail of personal data, consumers worry that government agencies or marketers could encroach on their privacy .

Ultimately, the book views e-money as a logical technological progression in the payments system that further reduces the “paper shuffling” costs associated with checks, even though infrastructure and security hurdles continue to slow its total adoption.

Measuring Money

In the book, measuring money is presented as the practical application of the theoretical concept that money is anything generally accepted as payment for goods or services. Within the larger context of “What Is Money?”, measurement is essential because a purely behavioral definition does not specify which specific assets in the economy should be counted for the purpose of conducting monetary policy.

The Federal Reserve’s Monetary Aggregates

The book explains that the Federal Reserve has developed two primary measures of the money supply, known as monetary aggregates, to track the various types of assets that function as money.

- M1: This is the narrowest measure of money and consists of the most liquid assets that can be used directly as a medium of exchange. Its components include currency (paper money and coins held by the nonbank public), traveler’s checks (not issued by banks), demand deposits (business checking accounts that do not pay interest), and other checkable deposits (interest-bearing household checking accounts).

- M2: This is a broader measure that includes all of M1 plus “near moneys”—assets that are not as liquid as those in M1 but can be converted into cash quickly at low cost. These additional components include small-denomination time deposits (CDs under $100,000), savings deposits, money market deposit accounts, and retail money market mutual fund shares.

The Importance of Precise Measurement

The book emphasizes that how money is measured matters significantly for understanding the economy. While the growth rates of M1 and M2 often move together, there have been critical periods where they diverged. For instance, between 1992 and 1994, M1 showed high growth while M2’s growth was much lower; conversely, from 2004 to 2007, M1 growth became negative while M2 growth increased slightly.

Measurement in the Context of Policy

In the broader discussion of “What Is Money?”, these aggregates are the tools used by policymakers to predict future economic performance. The book notes that when M1 and M2 send conflicting signals, it becomes difficult for the Federal Reserve to decide on the correct course of monetary policy. Ultimately, the book concludes that because no single aggregate is perfectly reliable, obtaining a precise and correct measure of money remains a vital challenge for economists and central bankers.

M1 Monetary Aggregate

In the book, M1 is defined as the narrowest measure of money reported by the Federal Reserve, consisting of the most liquid assets that can be used directly as a medium of exchange. Within the larger context of measuring money, M1 represents one of the primary “monetary aggregates” used by policymakers to track the money supply.

Components of M1

The book identifies four specific components that make up the M1 aggregate:

- Currency: This includes only paper money and coins in the hands of the nonbank public; it specifically excludes cash held in bank vaults or ATMs.

- Traveler’s Checks: This component counts only those traveler’s checks that are not issued by banks.

- Demand Deposits: These consist of business checking accounts that do not pay interest, as well as traveler’s checks issued by banks.

- Other Checkable Deposits: This item includes all other checkable deposits, primarily interest-bearing checking accounts held by households.

Liquidity and Practical Use

M1 is characterized as the most liquid measure because all its components are readily accepted for transactions. The book notes that these assets are “clearly money” because of their immediate utility as a medium of exchange. As of August 2014, the total value of M1 was approximately $2.8 trillion .

Role in Monetary Policy

The book emphasizes that measuring M1 is critical for conducting monetary policy, though it can be challenging because different aggregates sometimes send conflicting signals. While the growth rates of M1 and M2 (a broader measure) often move together, there have been periods of significant divergence. For example, from 2004 to 2007, the growth rate of M1 decelerated sharply and became negative, while the growth rate of M2 actually increased slightly. Such discrepancies mean that the choice of which aggregate to use as the “best” measure of money significantly impacts how economists and policymakers interpret the results of monetary policy.

M2 Monetary Aggregate

In the book, M2 is defined as a broad monetary aggregate that includes all of the liquid assets in M1 plus several other “near moneys” that are not quite as liquid but can be converted into cash quickly at low cost. Within the larger context of measuring money, M2 provides a more comprehensive view of the money supply than the narrower M1 aggregate, helping the Federal Reserve track assets that have check-writing features or can be turned into cash with little effort.

Components of M2

The M2 aggregate is calculated by adding the following components to the total value of M1 :

- Savings Deposits: These are nontransaction deposits that can be added to or withdrawn at any time.

- Money Market Deposit Accounts: These are similar to money market mutual funds but are issued specifically by banks.

- Small-Denomination Time Deposits: These consist of certificates of deposit (CDs) with a denomination of less than $100,000 that can only be redeemed without penalty at a fixed maturity date.

- Money Market Mutual Fund Shares (Retail): These are retail accounts on which households can write checks, essentially functioning as interest-paying checking accounts.

Liquidity and Measurement

The book notes that because various assets can function as money depending on how they are used, a single precise definition of the money supply is impossible. Consequently, the Federal Reserve uses M2 to capture assets that, while not used directly as a medium of exchange as frequently as M1 components, still influence economic behavior due to their high liquidity. As of August 2014, the total value of M2 was approximately $11.3 trillion, making it a much larger measure of the money supply than M1 .

M2 in the Context of Monetary Policy

The book emphasizes that measuring M2 is vital for predicting future economic performance and conducting monetary policy. While the growth rates of M1 and M2 often move together, they sometimes diverge significantly, sending conflicting signals to policymakers.

- Historical Divergence: Between 1992 and 1994, M1 experienced high growth while M2 grew much more slowly; conversely, from 2004 to 2007, M1 growth became negative while M2 growth increased slightly .

- Impact on Policy: Such discrepancies make it difficult for the Federal Reserve to determine the correct course of action, as one aggregate might suggest a need for tightening while the other suggests easing.

Ultimately, the book concludes that because no single aggregate is perfectly reliable, obtaining a precise and correct measure of money—and deciding whether to focus on M1 or M2—remains a fundamental challenge for economists and central bankers.

— Linden Lake

This series:

→ Book Review (1 of 3): The Economics of Money, Banking, and Financial Markets – Why Study This Topic?

→ Book Review (2 of 3): The Economics of Money, Banking, and Financial Markets – Overview the Financial Systems

→ Book Review (3 of 3): The Economics of Money, Banking, and Financial Markets – What is Money?

Leave a Reply