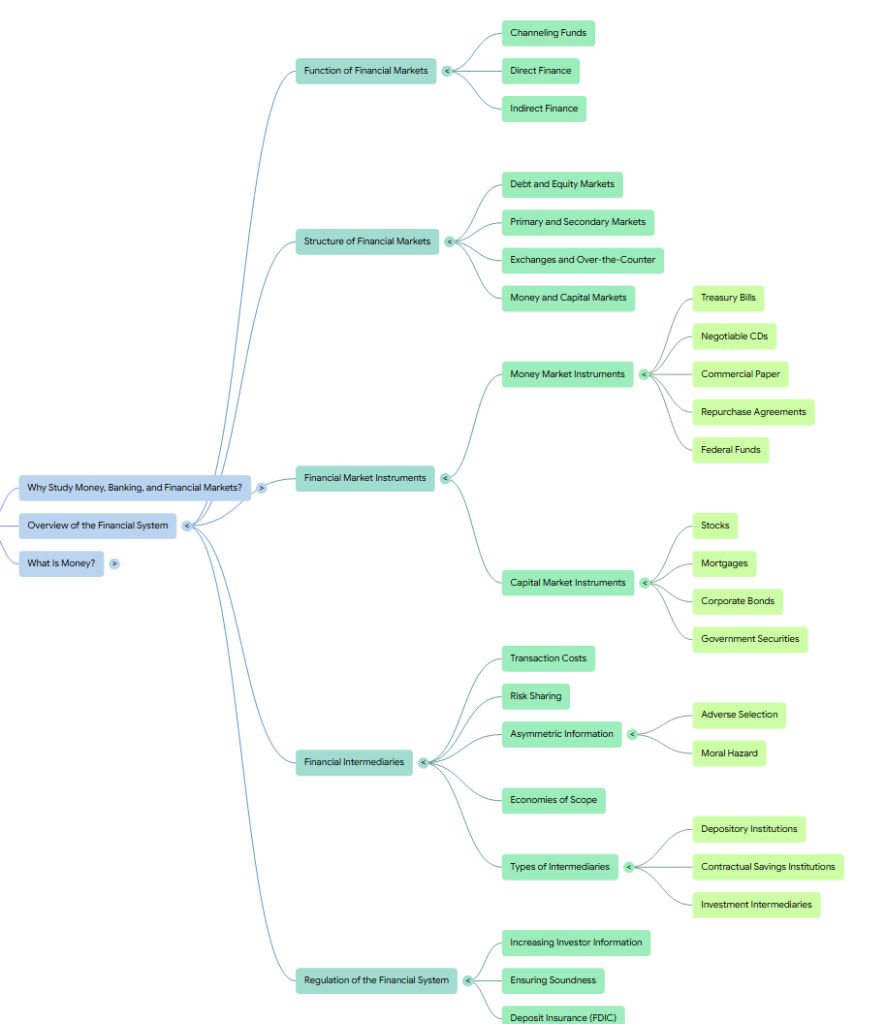

In the book, the overview of the financial system serves as a foundational pillar, explaining how funds move from those who have excess savings to those with productive investment opportunities. This process is vital because it promotes economic efficiency by ensuring that capital is allocated to its most productive uses, which in turn contributes to higher production and overall economic welfare.

The Core Function and Routes of Finance

The primary function of the financial system is to channel funds from “lender-savers” (typically households) to “borrower-spenders” (typically businesses and the government). The book identifies two distinct routes for this flow:

- Direct Finance: Borrowers obtain funds directly from lenders in financial markets by selling them securities (financial instruments), such as bonds or stocks. These securities represent a claim on the borrower’s future income or assets.

- Indirect Finance: This route involves a financial intermediary, such as a bank, which stands between the savers and the borrowers. The intermediary borrows from savers and then uses those funds to make loans to borrowers.

Structure of Financial Markets

The book categorizes financial markets based on several characteristics:

- Debt and Equity: Debt markets involve contractual agreements for fixed payments until a maturity date, while equity markets (stocks) represent ownership claims in a corporation.

- Primary and Secondary Markets: Primary markets handle the initial sale of new securities, often assisted by investment banks, whereas secondary markets involve the resale of previously issued securities. Secondary markets are essential because they provide liquidity to investors and determine the prices that firms receive for new securities in the primary market.

- Money and Capital Markets: Money markets deal in short-term debt instruments (maturity less than one year), which are generally more liquid and less risky. Capital markets trade longer-term debt and equity instruments.

- Internationalization: Modern financial markets are increasingly integrated, featuring instruments like Eurobonds (denominated in a currency other than that of the country where they are sold) and Eurodollars (U.S. dollars deposited in foreign banks).

The Economic Rationale for Financial Intermediaries

A central theme in the book is why indirect finance using financial intermediaries is often more important than direct finance. Intermediaries exist to solve three major problems:

- Transaction Costs: Institutions use expertise and economies of scale to reduce the time and money spent on financial transactions. They also provide liquidity services, such as checking accounts, that make it easier for customers to conduct business.

- Risk Sharing: Intermediaries engage in “asset transformation,” turning risky assets into safer ones for investors while helping individuals lower their risk through diversification.

- Asymmetric Information: Institutions are better equipped than individuals to handle situations where one party has superior information. They mitigate adverse selection (screening out bad risks before a transaction) and moral hazard (monitoring borrowers after a loan is made).

Types of Financial Intermediaries

The book classifies these institutions into three groups based on their sources and uses of funds:

- Depository Institutions (Banks): These include commercial banks, savings and loan associations, and credit unions that accept deposits and make various types of loans.

- Contractual Savings Institutions: Entities like insurance companies and pension funds that acquire funds at periodic intervals and invest in long-term securities.

- Investment Intermediaries: This group includes finance companies, mutual funds, and money market mutual funds.

Regulation of the Financial System

Because the financial system is critical to economic health, it is one of the most heavily regulated sectors. Regulation aims to increase the information available to investors—thereby reducing adverse selection and moral hazard—and to ensure the soundness of financial intermediaries to prevent damaging financial panics. Key regulatory tools include deposit insurance (FDIC), restrictions on asset holdings, and mandatory disclosure of financial information.

Function of Financial Markets

In the book, the primary function of financial markets is described as channeling funds from households, firms, and governments that have saved surplus funds (“lender-savers”) to those that have a shortage of funds (“borrower-spenders”). This process is essential to the health of the economy because the people who save are frequently not the same individuals who have productive investment opportunities. By facilitating the movement of funds to those with such opportunities, financial markets promote an efficient allocation of capital, which contributes to higher production and overall economic efficiency.

Routes of Finance

Within the overview of the financial system, the book identifies two distinct routes through which these funds flow:

- Direct Finance: In this route, borrowers obtain funds directly from lenders in financial markets by selling them securities (also known as financial instruments), which are claims on the borrower’s future income or assets.

- Indirect Finance: This route involves a financial intermediary that stands between the savers and the borrowers, borrowing from one to lend to the other. The book notes that indirect finance is actually the primary route for moving funds in the financial system.

Economic and Consumer Benefits

The book emphasizes that well-functioning financial markets are crucial for economic growth; conversely, poor-performing markets are a key reason many nations remain poor. Beyond macroeconomic efficiency, these markets directly improve the well-being of consumers by allowing them to better time their purchases. For example, financial markets provide the means for young people to buy homes and other necessities without having to wait until they have saved the entire purchase price.

Broader Context: Systemic Health

In the larger context of the financial system, the book explains that when these markets function efficiently, they improve the economic welfare of everyone in society. However, when financial markets break down during a financial crisis, as seen in the 2007–2009 global crisis, it results in severe economic hardship and can lead to dangerous political instability. Therefore, the structure of the financial system—comprising both markets and intermediaries—is designed to ensure that capital is directed toward its most productive uses while maintaining overall system stability.

Channeling Funds

In the book, the primary function of financial markets is the channeling of funds from entities that have saved surplus funds (lender-savers) to those that have a shortage of funds (borrower-spenders). This process is essential because the individuals who save are frequently not the same people who have productive investment opportunities.

The Direction of the Flow

The flow of funds typically moves from the left side of the financial system to the right:

- Lender-Savers: The principal savers are households, though business enterprises, governments, and foreigners also provide funds.

- Borrower-Spenders: The most important borrowers are businesses and the government (particularly the federal government), but households and foreigners also borrow to finance major purchases like houses or cars.

Two Routes for Channeling Funds

The book identifies two distinct paths through which these funds move:

- Direct Finance: In this route, borrowers obtain funds directly from lenders in financial markets by selling them securities (also called financial instruments). These securities represent claims on the borrower’s future income or assets.

- Indirect Finance: This route involves a financial intermediary, such as a bank, that stands between savers and borrowers. The intermediary borrows from the savers and then uses those funds to make loans to borrowers. This process of financial intermediation is the primary route for moving funds in the financial system.

Economic and Individual Importance

The book emphasizes that channeling funds is critical for several reasons:

- Productive Investment: It allows funds to move from people who lack productive investment opportunities to those who have them, such as “Carl the Carpenter” buying a new tool to increase his productivity.

- Economic Efficiency: By ensuring an efficient allocation of capital, financial markets contribute to higher production and overall efficiency for the entire economy.

- Consumer Well-Being: It allows consumers to better time their purchases. For example, it enables young people to buy a home and pay for it over time rather than waiting until they have saved the entire purchase price.

- Consequences of Failure: When the systems for channeling funds break down during a financial crisis, the result is severe economic hardship and potential political instability.

Direct Finance

In the book, direct finance is defined as the route through which borrowers obtain funds directly from lenders in financial markets by selling them securities (also known as financial instruments). These securities are assets for the person who buys them but liabilities (debts or IOUs) for the individual or firm that sells or issues them. This process is a key component of the broader function of financial markets, which is to channel funds from those who have saved surplus funds (lender-savers) to those who have a shortage of funds and a need for them (borrower-spenders).

The Role of Securities in Direct Finance

Direct finance typically involves the issuance of two main types of instruments:

- Debt Instruments: A contractual agreement where the borrower pays the holder fixed dollar amounts at regular intervals until a specified maturity date. A common example mentioned in the book is a bond.

- Equities: Claims to share in the net income and assets of a business, such as common stock. Unlike debt holders, equity holders often receive dividends and possess voting rights, though they are residual claimants who are paid only after all debt holders have been satisfied.

Market Structure for Direct Finance

The book distinguishes between different types of markets where direct finance occurs:

- Primary vs. Secondary Markets: A primary market is where new issues of a security are sold to initial buyers, often through an investment bank that underwrites the offering. A secondary market is where previously issued securities are resold, providing liquidity to investors and helping to determine the price of new securities in the primary market.

- Exchanges vs. Over-the-Counter (OTC) Markets: Direct finance can take place in centralized exchanges, like the New York Stock Exchange, or through OTC markets, where dealers at different locations stand ready to buy and sell securities to anyone willing to accept their prices.

Relative Importance and Limitations

While direct finance is highly visible, the book notes that it is many times less important than indirect finance (which involves financial intermediaries). In the United States, direct finance accounts for less than 10% of the external funding for American businesses.

The book explains that direct finance is often less accessible to individuals and small businesses due to several factors:

- Transaction Costs: Small savers often lack the funds or expertise to purchase securities directly because the time and money spent carrying out such transactions can be prohibitively high.

- Asymmetric Information: In direct financial markets, lenders often have less information about the potential returns and risks of a project than the borrower, leading to problems of adverse selection (before the transaction) and moral hazard (after the transaction).

- Access: Only large, well-established corporations typically have easy access to securities markets to finance their activities through direct finance.

Indirect Finance

In the book, indirect finance is described as the primary route for moving funds from lender-savers to borrower-spenders within the financial system. It involves the activity of a financial intermediary—such as a bank—that stands between the two parties, borrowing funds from savers by issuing liabilities and then using those funds to make loans to borrowers.

Prevalence and Importance

While the media often focuses on direct finance (the sale of stocks and bonds), the book emphasizes that indirect finance is many times more important. In the United States, direct finance accounts for less than 10% of the external funding for businesses, and in other developed nations like Germany and Japan, the reliance on indirect finance via financial intermediaries has historically been even higher.

The Role of Financial Intermediaries

Financial intermediaries are essential to the function of financial markets because they reduce the frictions that otherwise prevent funds from flowing to productive investment opportunities. The book identifies three key reasons why indirect finance is so effective:

- Transaction Costs: Intermediaries reduce the time and money spent on financial transactions by utilizing economies of scale. For example, a bank can hire one lawyer to produce an airtight loan contract that is used for thousands of loans, reducing the legal cost per individual transaction to a negligible amount.

- Risk Sharing: Intermediaries engage in asset transformation, where they create and sell assets with risk characteristics that investors find comfortable and then use those proceeds to buy riskier assets. They also facilitate diversification, allowing individual savers to pool their money to hold a collection of assets, which lowers their overall risk exposure.

- Asymmetric Information: Indirect finance is particularly suited to solving problems where one party has superior information compared to the other.

- Adverse Selection: Intermediaries are experts at screening potential borrowers before a transaction to sort out good credit risks from bad ones.

- Moral Hazard: After a loan is made, intermediaries have the expertise to monitor the borrower’s activities to ensure they do not engage in risky behavior that would make them unable to repay the loan.

The Role of Banks

Banks are highlighted as the most important source of external funds for businesses because they primarily make private, nontraded loans. By keeping these loans private, banks avoid the free-rider problem that plagues securities markets; other investors cannot observe the bank’s information-gathering and monitoring activities and bid away the bank’s profit. Consequently, the book notes that the lending role of these institutions is vital for an economy to reach its full potential.

Structure of Financial Markets

In the book, the structure of financial markets is categorized in several ways to explain how funds are channeled from lender-savers to borrower-spenders. These markets are a vital component of the financial system, providing the framework through which both direct and indirect finance occur.

Debt and Equity Markets

A firm or individual can obtain funds in a financial market through two primary methods:

- Debt Instruments: The most common method involves issuing a debt instrument, such as a bond or mortgage, which is a contractual agreement to pay the holder fixed dollar amounts at regular intervals until a specified maturity date. Maturity is classified as short-term (less than a year), intermediate-term (one to ten years), or long-term (ten years or longer).

- Equities: This method involves issuing claims to share in the net income and assets of a business, such as common stock. Equity holders are residual claimants, meaning the corporation must pay all debt holders before paying them, but they benefit directly from increases in profitability or asset value.

Primary and Secondary Markets

The book distinguishes between markets based on whether the securities being traded are new or previously issued:

- Primary Market: A market in which new issues of a security are sold to initial buyers. These transactions often take place “behind closed doors” and typically involve an investment bank that underwrites the securities by guaranteeing a price and selling them to the public.

- Secondary Market: A market in which previously issued securities can be resold, such as the New York Stock Exchange or NASDAQ. These markets serve two critical functions: they make financial instruments more liquid and they determine the price at which the issuing firm can sell new securities in the primary market.

Exchanges and Over-the-Counter (OTC) Markets

Secondary markets are organized in two distinct ways:

- Exchanges: Centralized locations where buyers and sellers (or their agents) meet to conduct trades, such as the New York Stock Exchange.

- Over-the-Counter (OTC) Markets: Markets where dealers at different locations stand ready to buy and sell securities to anyone willing to accept their prices via computer contact. The book notes that the U.S. government bond market, which has a larger trading volume than the NYSE, is an OTC market.

Money and Capital Markets

Finally, the book differentiates markets based on the maturity of the securities traded:

- Money Market: A market that deals exclusively in short-term debt instruments (original maturity of less than one year). These securities are generally more liquid and safer than longer-term instruments, making them ideal for banks and corporations to earn interest on temporary surplus funds.

- Capital Market: A market for longer-term debt (maturity of one year or greater) and equity instruments. These assets, such as stocks and long-term bonds, are often held by institutions like insurance companies and pension funds that have more certainty about their future fund availability.

Debt and Equity Markets

In the book, the structure of financial markets is categorized in several ways, with the primary distinction being how a firm or individual obtains funds: through the issuance of debt instruments or through the issuance of equities.

Debt Markets

Debt instruments, such as bonds or mortgages, are contractual agreements where the borrower agrees to pay the holder fixed dollar amounts at regular intervals (interest and principal) until a specified maturity date. The book classifies these instruments based on their term to maturity:

- Short-term: Maturity of less than one year.

- Intermediate-term: Maturity between one and ten years.

- Long-term: Maturity of ten years or longer.

The debt market is a massive component of the financial system; at the end of 2013, the value of debt instruments in the United States was $42 trillion, nearly double the $21.3 trillion value of equities.

Equity Markets

Equities, such as common stock, represent claims to share in the net income and the assets of a business. Key characteristics include:

- Dividends: Periodic payments made to holders.

- Maturity: Considered long-term securities because they have no maturity date.

- Rights: Ownership typically grants the right to vote on important issues and elect directors.

- Residual Claimant Status: A significant disadvantage is that the corporation must pay all debt holders before paying equity holders. Conversely, the advantage is that equity holders benefit directly from any increase in the firm’s profitability or asset value.

The Context of Financial Structure and Information

The book places these markets within the broader context of asymmetric information and moral hazard:

- Principal-Agent Problem: Equity contracts are particularly susceptible to this type of moral hazard, where managers (agents) may act in their own interest rather than the interest of the stockholder-owners (principals).

- Monitoring and Verification: One reason debt contracts are more common for raising capital is that they require less frequent monitoring than equity contracts. Lenders only need to verify a firm’s state (costly state verification) when the firm cannot meet its fixed debt payments.

- Moral Hazard in Debt: While debt reduces some monitoring needs, it still faces moral hazard because borrowers have incentives to take on riskier projects than lenders would prefer, since they keep any profits exceeding the fixed debt payment.

Place within Market Classifications

Debt and equity markets are further structured into:

- Money vs. Capital Markets: Money markets deal exclusively in short-term debt instruments, while capital markets trade longer-term debt and equity instruments.

- Primary vs. Secondary Markets: New issues of debt or equity are sold in primary markets, while previously issued securities are resold in secondary markets, which provide liquidity and determine the pricing for new issues.

Primary and Secondary Markets

In the book, financial markets are categorized by whether the securities being traded are new or have been previously issued, leading to the distinction between primary and secondary markets.

Primary Markets

A primary market is a financial market in which a corporation or government agency borrowing funds sells new issues of securities, such as bonds or stocks, to initial buyers. The book notes that these markets are often not well known to the public because the sale of these securities frequently takes place “behind closed doors”. A key institution in the primary market is the investment bank, which assists in the initial sale by underwriting the securities—guaranteeing a price for the issuing firm and then selling them to the public.

Secondary Markets

A secondary market is a financial market where securities that have been previously issued are resold. Familiar examples include the New York Stock Exchange and NASDAQ, although the book points out that bond markets actually have a larger trading volume. Two types of participants are essential to a well-functioning secondary market:

- Brokers: Agents of investors who match buyers with sellers of securities.

- Dealers: Participants who link buyers and sellers by buying and selling securities at stated prices.

The Context of Financial Market Structure

While firms only acquire new funds when their securities are first sold in the primary market, the book emphasizes that secondary markets are critical to the overall structure of the financial system for two primary reasons:

- Liquidity: They make financial instruments more liquid by making them easier and quicker to sell for cash. This increased liquidity makes securities more desirable to investors, which subsequently makes them easier for issuing firms to sell in the primary market.

- Pricing: They determine the price of the securities that issuing firms sell in the primary market. Initial buyers will pay no more for a new security than the price they expect the secondary market to set for it; thus, the higher the secondary market price, the more capital a firm can raise in the primary market.

Within the broader structure of financial markets, the book also classifies secondary markets by their organization. They can be exchanges, where buyers and sellers meet in a central location, or over-the-counter (OTC) markets, where dealers at different locations stand ready to trade via computer contact. These categories interact with other structural elements, such as whether the securities are traded in money markets (short-term) or capital markets (long-term), and whether they are debt or equity instruments.

Exchanges and Over-the-Counter

In the book, exchanges and over-the-counter (OTC) markets are identified as the two primary ways in which secondary financial markets are organized. This categorization is a key component of the broader structure of financial markets, which also includes distinctions between debt and equity markets, primary and secondary markets, and money and capital markets.

Organized Exchanges

The book defines an exchange as a centralized location where buyers and sellers of securities, or their agents and brokers, meet to conduct trades.

- Examples: Well-known examples include the New York Stock Exchange (NYSE) for stocks and the Chicago Board of Trade for commodities such as wheat, corn, and silver.

- Function: While many large corporations have their shares traded on these organized exchanges, they represent only one portion of the total trading activity in the financial system.

Over-the-Counter (OTC) Markets

In contrast to a centralized exchange, an over-the-counter market is a decentralized forum where dealers at various locations maintain an inventory of securities and stand ready to buy and sell them to anyone willing to accept their prices.

- Competitive Nature: Although dealers are in different locations, they are in constant contact via computers and are aware of the prices set by one another. As a result, the book notes that OTC markets are very competitive and function similarly to organized exchanges.

- Examples and Scope: Many common stocks are traded over-the-counter. Significantly, the book points out that the U.S. government bond market—which has a larger trading volume than the New York Stock Exchange—is organized as an OTC market. Other examples of OTC markets include those for negotiable certificates of deposit, federal funds, and foreign exchange instruments.

Context within Financial Market Structure

The distinction between exchanges and OTC markets specifically applies to the organization of secondary markets, where previously issued securities are resold. The book emphasizes that while corporations do not acquire new funds in these markets, the organization of secondary markets is vital for two reasons:

- Liquidity: They make financial instruments more liquid, meaning they are easier and quicker to sell for cash, which makes them more desirable to investors.

- Pricing: They establish the prices for securities, which directly determines the amount of funds a corporation can raise when selling new issues in the primary market.

Ultimately, whether a secondary market is organized as a centralized exchange or a decentralized OTC market, its primary role in the structure of the financial system is to facilitate the efficient trading and valuation of existing securities.

Money and Capital Markets

In the book, financial markets are categorized by the maturity of the securities traded in them, resulting in the distinction between money markets and capital markets. This classification is a key element in the broader structure of financial markets, which also encompasses distinctions between debt and equity, primary and secondary markets, and organized exchanges versus over-the-counter markets.

Money Markets

The money market is defined as a financial market in which only short-term debt instruments—generally those with an original maturity of less than one year—are traded.

- Characteristics: These securities are usually more widely traded and therefore tend to be more liquid than longer-term securities. They also experience smaller price fluctuations, making them safer investments.

- Purpose: Because of their safety and liquidity, corporations and banks actively use the money market to earn interest on surplus funds they expect to hold only temporarily.

- Primary Instruments: Key instruments include U.S. Treasury bills, negotiable bank certificates of deposit (CDs), commercial paper, repurchase agreements (repos), and federal funds.

Capital Markets

The capital market is the market in which longer-term debt (original maturity of one year or greater) and equity instruments are traded.

- Characteristics: Capital market instruments often exhibit far wider price fluctuations than money market instruments and are generally considered to be riskier investments.

- Purpose: These securities are typically held by financial intermediaries, such as insurance companies and pension funds, which have more certainty about the amount of funds they will need in the future.

- Primary Instruments: Key instruments include stocks (equities), residential and commercial mortgages, mortgage-backed securities, corporate bonds, U.S. government and agency securities, state and local government (municipal) bonds, and consumer and bank commercial loans.

Context Within the Financial Structure

The book emphasizes that while the average person is often more aware of the stock market (a major component of the capital market), the debt market is substantially larger; for example, at the end of 2013, the value of debt instruments in the U.S. was nearly double that of equities. Furthermore, while businesses raise new funds in the primary market, the secondary market—where these money and capital market instruments are resold—is vital for providing the liquidity and pricing information necessary for the primary market to function effectively. Together, these markets perform the essential economic function of channeling funds from those with excess savings to those with productive investment opportunities.

Financial Market Instruments

In the book, financial market instruments (also called securities) are defined as claims on the issuer’s future income or assets. These instruments are the essential vehicles used to perform the core function of the financial system: channeling funds from lender-savers to borrower-spenders. Within the overview of the financial system, the book categorizes these instruments based on their maturity into two distinct groups: money market instruments and capital market instruments.

Money Market Instruments

The money market deals in short-term debt instruments with original maturities of less than one year. Because of their short terms, these instruments undergo the least price fluctuations and are considered the least risky investments in the financial system. Principal instruments include:

- U.S. Treasury Bills: One-, three-, and six-month debt instruments issued by the federal government; they are the most liquid and safest money market instruments because they have almost no risk of default .

- Negotiable Bank Certificates of Deposit (CDs): Debt instruments sold by banks to depositors that pay annual interest and can be resold in secondary markets.

- Commercial Paper: Short-term debt instruments issued by large banks and well-known corporations, such as Microsoft or General Motors.

- Repurchase Agreements (Repos): Effectively short-term loans (usually less than two weeks) where Treasury bills serve as collateral.

- Federal (Fed) Funds: Typically overnight loans between banks of their deposits at the Federal Reserve.

Capital Market Instruments

Capital market instruments are debt and equity instruments with maturities greater than one year. They generally experience wider price fluctuations and are considered riskier than money market instruments. Key instruments include:

- Stocks: Equity claims on the net income and assets of a corporation; at the end of 2013, the value of stocks exceeded that of any other capital market security.

- Mortgages and Mortgage-Backed Securities: Loans to households or firms to purchase land or structures, often bundled into bond-like instruments (mortgage-backed securities).

- Corporate Bonds: Long-term bonds issued by corporations with strong credit ratings; while the market is smaller than the stock market, the volume of new issues is often much greater .

- U.S. Government Securities: Long-term debt instruments issued by the U.S. Treasury to finance federal deficits; they are the most liquid securities in the capital market.

- U.S. Government Agency Securities: Long-term bonds issued by various government agencies (like “Ginnie Mae”) to finance items such as mortgages or farm loans.

- State and Local Government Bonds: Also called municipal bonds, these are issued to finance expenditures on schools and roads; their interest payments are notably exempt from federal income tax.

- Consumer and Bank Commercial Loans: Loans made principally by banks to consumers and businesses.

Context within the Financial System

The book emphasizes that these instruments are critical for producing an efficient allocation of capital, allowing funds to move from those who lack productive investment opportunities to those who have them. In the broader context of the financial system, these instruments can be traded through direct finance, where borrowers sell securities directly to lenders in financial markets, or indirect finance, where financial intermediaries like banks or mutual funds acquire these instruments using funds obtained from savers . Furthermore, the book notes a growing trend toward the internationalization of these instruments, with the rise of Eurobonds and Eurodollars reflecting the increasingly integrated nature of global financial markets.

Money Market Instruments

The book defines financial market instruments, also known as securities, as claims on the issuer’s future income or assets. These instruments are categorized into two primary groups based on their maturity: money market instruments and capital market instruments. Money market instruments are short-term debt instruments with original maturities of less than one year, whereas capital market instruments include longer-term debt and equity instruments with maturities of one year or more.

Because of their short duration, money market instruments undergo the least price fluctuations and are consequently viewed as the least risky investments in the financial system. They are usually more widely traded and more liquid than longer-term securities. The book notes that corporations and banks actively use these instruments to earn interest on surplus funds they expect to hold only temporarily.

The book identifies several principal money market instruments:

- U.S. Treasury Bills: These are short-term debt instruments issued by the federal government in one-, three-, and six-month maturities. They are considered the most liquid and safest money market instruments because they have almost no risk of default. They do not pay interest directly but are sold at a discount from their face value.

- Negotiable Bank Certificates of Deposit (CDs): These are debt instruments sold by banks to depositors that pay annual interest and return the original purchase price at maturity. Unlike non-negotiable CDs, these can be resold in secondary markets, making them an important source of funds for commercial banks from entities like money market mutual funds.

- Commercial Paper: This is a short-term debt instrument issued by large banks and well-known corporations. Improvements in information technology have made it easier for investors to screen credit risks, leading to significant growth in this market as corporations bypass banks to borrow short-term funds directly from the public.

- Repurchase Agreements (Repos): These function as short-term loans, usually with a maturity of less than two weeks, for which Treasury bills serve as collateral. In these transactions, a lender (often a large corporation) purchases T-bills from a bank, which agrees to repurchase them at a slightly higher price in the near future.

- Federal (Fed) Funds: These are typically overnight loans between banks of their deposits held at the Federal Reserve. The interest rate on these loans, the federal funds rate, is a sensitive barometer of the tightness of credit conditions in the banking system and the stance of monetary policy.

In the larger context of financial market instruments, these money market vehicles are essential for the efficient allocation of capital, allowing funds to move to those with productive investment opportunities. While they are part of the broader category of securities that includes riskier and more volatile capital market instruments like stocks and long-term bonds, money market instruments provide the specialized function of managing short-term liquidity and safety for the entire financial system.

Treasury Bills

The book defines money market instruments as short-term debt instruments with original maturities of less than one year. Because of their short duration, these instruments undergo the smallest price fluctuations and are considered the least risky and most liquid investments in the financial system. Within this category, U.S. Treasury bills are highlighted as the most important and fundamental instrument.

Characteristics of Treasury Bills

U.S. Treasury bills are short-term debt instruments issued by the federal government in one-, three-, and six-month maturities to finance its operations. Unlike many other securities, they do not make periodic interest payments. Instead, they pay interest effectively by selling at a discount—that is, at a price lower than the face value paid at maturity. For example, an investor might purchase a six-month bill for $9,000 and redeem it for its $10,000 face value upon maturity.

Role as the Benchmark Instrument

The book identifies two primary reasons why Treasury bills are the preeminent money market instrument:

- Liquidity: They are the most liquid of all money market instruments because they are the most actively traded, making them easy and inexpensive to convert into cash.

- Safety: They are considered the safest money market instrument because there is an extremely low probability of default. The book notes that the federal government can always meet its debt obligations by raising taxes or issuing currency.

Holders and Market Usage

Treasury bills are held primarily by banks, though households, corporations, and other financial intermediaries also hold them as a way to earn interest on temporary surplus funds. In the broader money market context, they are so widely trusted that they often serve as collateral for other transactions. For instance, in a repurchase agreement (repo), a large corporation may effectively lend funds to a bank by purchasing Treasury bills, which the bank agrees to buy back at a slightly higher price in the near future.

Importance in the Financial System

The interest rate on three-month Treasury bills is one of the most frequently reported money market rates and serves as a sensitive indicator of general interest-rate movements and credit market conditions. Historically, these rates have seen substantial fluctuations, peaking at over 16% in 1981 before falling to near zero in the years following the 2008 financial crisis. Despite these fluctuations, they remain a critical tool for both government finance and private liquidity management.

Negotiable CDs

In the book, negotiable bank certificates of deposit (CDs) are identified as a principal money market instrument, functioning as debt instruments sold by banks to depositors that pay annual interest and return the original purchase price at maturity. Unlike non-negotiable CDs, these are traded in secondary markets, which allows them to be resold before they mature.

Characteristics and Holders

The book notes that negotiable CDs are large-denomination time deposits, typically available in amounts of $100,000 or more. Because of their large size and the ability to be resold, they are primarily held by:

- Corporations: They use these instruments to earn interest on temporary surplus funds.

- Money Market Mutual Funds: These funds purchase negotiable CDs as safe, liquid assets to hold in their portfolios.

- Other Institutions: Charitable institutions and government agencies also utilize them as a source of short-term investment.

Currently, the amount of negotiable CDs outstanding is approximately $1.8 trillion, making them an essential source of funds for commercial banks.

Context within Money Market Instruments

As part of the broader category of money market instruments, negotiable CDs share several key traits with vehicles like U.S. Treasury bills and commercial paper:

- Short Maturity: They generally have original maturity terms of less than one year.

- High Liquidity: Because they are widely traded in secondary markets, they are highly liquid and can be converted into cash quickly.

- Low Risk: Their short duration means they undergo smaller price fluctuations compared to long-term capital market instruments, making them safer investments.

Historical Significance and Liability Management

The book emphasizes that the introduction of negotiable CDs in 1961 was a watershed moment for the banking industry. Prior to the 1960s, banks primarily engaged in asset management, treating their liabilities as fixed. Starting in the 1960s, however, large money center banks used negotiable CDs to pioneer liability management.

By selling these instruments, banks no longer had to rely solely on checkable deposits; instead, they could aggressively acquire funds as needed to take advantage of attractive loan opportunities. This shift is reflected in the changing composition of bank balance sheets, where negotiable CDs and other borrowings have risen from only 2% of bank liabilities in 1960 to 31% by mid-2014.

Commercial Paper

In the book, commercial paper is identified as a major money market instrument, functioning as a short-term debt security issued by large banks and well-known, high-quality corporations such as Microsoft and General Motors. Within the larger context of money market instruments, commercial paper is part of a category of debt assets with original maturities of less than one year that are generally characterized by high liquidity and low risk.

Growth and Technological Influence

The book highlights the remarkable growth of the commercial paper market, noting that the amount outstanding increased by over 700% between 1980 and 2013, rising from $122 billion to $951 billion. This expansion was primarily driven by improvements in information technology, which made it significantly easier for investors to screen the credit risk of corporations. As a result, many large firms found it cheaper to raise short-term funds by issuing commercial paper directly to the public rather than taking out traditional bank loans.

Role of Institutional Investors

A key factor in the market’s stability and growth is the role of money market mutual funds. Because these funds must hold liquid, high-quality, short-term assets to meet their own shareholders’ needs, they have become a primary and ready market for commercial paper. The book notes that the proliferation of these funds, which held around $2.7 trillion in assets as of 2013, has provided a steady stream of demand for the instrument.

Strategic Use and Financial Distress

While typically a stable market, commercial paper can be sensitive to broader financial frictions. For example, during the global financial crisis of 2007–2009, the commercial paper market experienced severe disruptions. To prevent a complete collapse of this funding source for corporations, the Federal Reserve stepped in with the Commercial Paper Funding Facility (CPFF) in October 2008 to finance the purchase of commercial paper directly from issuers.

Context in the Financial System

As a money market instrument, commercial paper serves as a critical tool for liquidity management. It allows corporations with temporary surplus funds to earn interest by lending to other well-established firms that require short-term financing. By enabling this direct transfer of funds, commercial paper contributes to the overall efficiency of the financial system by lowering transaction costs and bypassing the traditional banking intermediary.

Repurchase Agreements

In the book, repurchase agreements (repos) are identified as a principal money market instrument, functioning effectively as short-term loans with maturities typically lasting less than two weeks. Within the larger context of money market instruments, repos are part of a category of short-term debt assets that undergo minimal price fluctuations and are considered among the safest and most liquid investments in the financial system.

Mechanism and Participants

The book explains that a repo transaction involves a lender (often a large corporation with temporary idle funds) purchasing U.S. Treasury bills from a borrower (usually a bank). The borrower agrees to repurchase these securities in the near future—often only a week later—at a price slightly higher than the original purchase price. The difference in price represents the interest on the loan, and the Treasury bills serve as collateral, which the lender receives if the borrower fails to repay. Large corporations have become the most important lenders in this market, providing an essential source of funds for commercial banks.

Use in Monetary Policy

The Federal Reserve utilizes repurchase agreements as a primary tool for conducting defensive open market operations.

- Repos: When the Fed wishes to conduct a temporary open market purchase to increase reserves, it buys securities with an agreement that the seller will repurchase them in a short period (one to fifteen days).

- Matched Sale-Purchase Transactions: Also known as reverse repos, these occur when the Fed sells securities and the buyer agrees to sell them back to the Fed in the near future. This serves as a temporary open market sale to drain reserves from the banking system.

Role in the Financial Crisis

The book notes that repurchase agreements were central to the “run on the shadow banking system” during the global financial crisis of 2007–2009. As concerns about the quality of financial institutions’ balance sheets grew, lenders began requiring larger amounts of collateral for repo loans, a practice known as increasing haircuts. For example, a 5% haircut meant a borrower had to post $105 million in assets to secure a $100 million loan. When these haircuts rose sharply—sometimes to nearly 50%—financial institutions were forced to engage in fire sales of assets to raise cash, leading to massive deleveraging and a severe contraction in economic activity.

Federal Funds

In the book, federal funds are defined as typically overnight loans between banks of their deposits held at the Federal Reserve. Despite the name, these loans are not made by the federal government or the Fed itself, but rather by one private bank to another.

Function and Mechanism

The primary reason a bank enters the federal funds market is to meet reserve requirements. If a bank finds that its deposit accounts at the Fed fall below the amount required by regulators, it can borrow the necessary funds from another bank that has a surplus. These funds are then transferred using the Federal Reserve’s wire transfer system.

The Federal Funds Rate as an Indicator

The interest rate charged on these overnight loans is known as the federal funds rate. The book identifies this rate as a “closely watched barometer” for two main reasons:

- Credit Market Tightness: A high federal funds rate indicates that banks are “strapped for funds,” while a low rate suggests their credit needs are low.

- Monetary Policy Stance: It serves as a sensitive indicator of the current stance of monetary policy. Because of its significance, it is one of the four money market rates most frequently reported in the media .

Context within Money Market Instruments

Federal funds are categorized as one of the principal money market instruments, which are short-term debt instruments with original maturities of less than one year .

- Risk and Liquidity: Like other money market instruments—such as U.S. Treasury bills and commercial paper—federal funds undergo the least price fluctuations and are considered among the least risky investments in the financial system.

- Market Growth: The book notes significant growth in this sector; when combined with security repurchase agreements, the amount outstanding grew from $64 billion in 1980 to $1,919 billion by the end of 2013 .

In the broader structure of the financial system, federal funds represent a vital component of the over-the-counter (OTC) market, where dealers at different locations stay in constant contact via computer to buy and sell these instruments.

Capital Market Instruments

In the book, capital market instruments are defined as debt and equity instruments with original maturities of one year or greater. Within the broader category of financial market instruments (securities), they are distinguished from money market instruments by their longer duration, which typically leads to far wider price fluctuations and a higher degree of risk.

Core Function and Characteristics

While money market instruments are used by banks and corporations to manage temporary surpluses of funds, capital market instruments are often held by financial intermediaries—such as insurance companies and pension funds—that have more certainty about their future funding needs. These instruments are essential for the long-term channeling of funds from lender-savers to borrower-spenders for productive investment.

Principal Capital Market Instruments

The book identifies several key instruments that comprise the capital market:

- Stocks: These are equity claims on the net income and assets of a corporation. At the end of 2013, the market value of stocks ($21.4 trillion) exceeded that of any other type of capital market security . They are primarily held by individuals, though pension funds, mutual funds, and insurance companies also hold large amounts.

- Mortgages and Mortgage-Backed Securities (MBS): Mortgages are loans to households or firms to purchase land or structures, using the property itself as collateral. The mortgage market is the largest debt market in the United States. Mortgage-backed securities are bond-like instruments backed by bundles of individual mortgages, which played a notorious role in the 2007–2009 global financial crisis.

- Corporate Bonds: These are long-term bonds issued by corporations with strong credit ratings. While the overall market size is smaller than the stock market, the volume of new corporate bond issues is substantially greater each year, making them critical to firm financing decisions.

- U.S. Government Securities: These are long-term debt instruments issued by the U.S. Treasury to finance federal deficits. Because they are so widely traded, they are considered the most liquid securities in the capital market.

- U.S. Government Agency Securities: These are long-term bonds issued by agencies like “Ginnie Mae” to finance specific items such as mortgages or farm loans. Many are guaranteed by the federal government.

- State and Local Government Bonds (Municipal Bonds): These are long-term debt instruments used to finance expenditures on schools, roads, and other programs. Their defining feature is that interest payments are exempt from federal income tax; consequently, commercial banks are the largest buyers.

- Consumer and Bank Commercial Loans: These are loans made principally by banks to businesses and consumers.

Comparative Risk and Liquidity

The book emphasizes that capital market instruments are generally less liquid and riskier than money market instruments. For example, corporate bonds are not nearly as liquid as U.S. government bonds because the outstanding amount for any single corporation is relatively small. Furthermore, equity holders are “residual claimants,” meaning they are only paid after all debt holders have been satisfied, which adds a layer of risk not present in debt instruments.

Stocks

In the book, stocks (specifically common stock) are defined as securities representing a share of ownership in a corporation and claims on the earnings and assets of that business. Within the larger context of capital market instruments, which are debt and equity instruments with maturities of one year or greater, stocks are considered long-term securities because they have no specific maturity date.

Characteristics and Ownership Rights

The book outlines several key features that distinguish stocks from other capital market instruments:

- Dividends: Stockholders may receive periodic payments from the net earnings of the corporation, though these are not guaranteed.

- Voting Rights: Unlike debt holders, owners of common stock typically have the right to vote on important issues and elect the board of directors.

- Residual Claimant Status: A significant characteristic of equity is that stockholders are residual claimants; the corporation must satisfy all claims by debt holders before paying its equity holders.

- Potential for Gain: While they carry more risk, equity holders benefit directly from any increase in the corporation’s profitability or asset value, whereas debt holders generally receive fixed payments.

Stocks in the Capital Market

The book places stocks alongside other major capital market instruments such as corporate bonds, residential and commercial mortgages, and U.S. government securities .

- Market Importance: Although the debt market is often larger in total value (in 2013, $42 trillion in debt versus $21.3 trillion in equities), the stock market is the most widely followed financial market.

- Market Value: At the end of 2013, the market value of stocks exceeded that of any other single type of security in the capital market .

- Volatility: Capital market instruments, particularly stocks, exhibit much wider price fluctuations and are considered riskier than short-term money market instruments.

- Primary vs. Secondary Markets: While corporations raise new funds in the primary market, the book notes that the volume of new stock issues in any given year is typically less than 1% of the total value of shares outstanding. Most stock trading occurs in secondary markets like the NYSE or NASDAQ, which provide liquidity and set the pricing for new issues.

Valuation and Dynamics

The book explains that the value of a stock is determined by the present value of all its future cash flows, which primarily consist of dividends. Models like the Gordon growth model are used to estimate these values based on expected dividend growth and the required return on equity.

The book also emphasizes the role of expectations and information in the stock market. According to the efficient market hypothesis, stock prices reflect all available information, meaning that future changes in prices should be unpredictable and follow a “random walk”. Because market participants constantly receive and react to new information—such as changes in monetary policy or economic conditions during a financial crisis—stock prices remain extremely volatile.

Mortgages

In the book, mortgages are categorized as a primary type of capital market instrument, which are debt and equity instruments with original maturities of one year or greater. Within this broader context, mortgages represent the largest debt market in the United States .

Mortgages as Capital Market Instruments

Capital market instruments are characterized by wider price fluctuations and higher risk compared to short-term money market instruments. Mortgages, specifically, are loans provided to households or firms to purchase land, housing, or other real structures, with the property itself serving as collateral for the loan.

The book distinguishes several key features of the mortgage market:

- Scale and Scope: The value of residential mortgages is more than quadruple that of commercial and farm mortgages.

- Primary Providers: Traditional providers include commercial banks, savings and loan associations, mutual savings banks, and insurance companies .

- Government Involvement: Federal agencies such as “Fannie Mae” (FNMA), “Ginnie Mae” (GNMA), and “Freddie Mac” (FHLMC) play an active role by selling bonds to purchase mortgages, thereby providing liquidity to the market.

Mortgage-Backed Securities (MBS)

A significant evolution in this capital market sector is the rise of mortgage-backed securities. These are bond-like debt instruments backed by a bundle of individual mortgages, where interest and principal payments are collectively paid out to the security holders. This process, known as securitization, allowed illiquid individual mortgages to be transformed into marketable capital market instruments.

Role in the Global Financial Crisis

The book emphasizes that mortgages, particularly subprime mortgages—loans offered to borrowers with less-than-stellar credit records—were a central trigger of the 2007–2009 global financial crisis.

- Financial Innovation: Improvements in information technology and data mining (such as FICO scores) made it easier to bundle subprime mortgages into securities.

- The Shadow Banking System: This process led to an “originate-to-distribute” model where mortgage brokers (originators) had weak incentives to evaluate a borrower’s ability to pay, as the loans were quickly sold off to be bundled into complex securities like MBS and collateralized debt obligations (CDOs).

- The Housing Bubble: When housing prices crashed in 2006, many subprime borrowers found their mortgages were “underwater,” leading to a surge in defaults and the subsequent collapse of the value of these capital market instruments.

Economic Rationale: Collateral and Asymmetric Information

From a structural perspective, mortgages are essential because they utilize collateral to reduce the problems of asymmetric information. By pledging the property as compensation in the event of default, the lender’s risk of adverse selection and moral hazard is mitigated, making it more likely that credit will be extended to households and firms. However, the book notes that in many developing countries, the “tyranny of collateral”—caused by the high cost or legal difficulty of obtaining property titles—prevents the poor from accessing the mortgage market to finance businesses or homes .

Corporate Bonds

In the book, corporate bonds are categorized as a major type of capital market instrument, which are debt and equity instruments with original maturities of one year or greater. Within this broader category, corporate bonds represent a vital mechanism for well-established firms to raise long-term capital for their operations.

Characteristics and Types

The book describes the typical corporate bond as a long-term debt instrument issued by a corporation with a very strong credit rating. These bonds generally pay the holder interest twice a year and return the full face value when the bond reaches its maturity date.

A specific variant mentioned is the convertible bond. These have an added feature that allows the holder to convert the bond into a specified number of shares of stock at any time before maturity. This feature makes the bonds more attractive to investors, as they can benefit if the company’s stock price rises, and it allows the issuing corporation to pay a lower interest rate.

Market Dynamics and Importance

Although the total market value of outstanding corporate bonds is significantly smaller than that of the stock market—amounting to less than one-third of the value of stocks—the book emphasizes their importance in a different way. The volume of new corporate bond issues in any given year is substantially greater than the volume of new stock issues. Consequently, the behavior of the corporate bond market is often considered more critical to a firm’s financing decisions than the behavior of the stock market.

Liquidity and Risk

In the context of the wider capital market, corporate bonds are distinguished by their level of risk and liquidity:

- Liquidity: Corporate bonds are not nearly as liquid as U.S. government bonds. This is because the total amount of bonds outstanding for any single corporation is relatively small, making them harder to sell quickly in an emergency without incurring high costs.

- Risk: Like all capital market instruments, corporate bonds experience wider price fluctuations and higher risk than short-term money market instruments. Within the risk structure of interest rates, they carry a risk premium—a higher interest rate than default-free U.S. Treasury bonds—to compensate investors for the possibility that the corporation might default .

Principal Holders

The primary buyers of corporate bonds are life insurance companies, which hold them to match their long-term liabilities. Other significant holders include pension funds and households. This illustrates the role of financial intermediaries in the “indirect finance” route, where these institutions use the funds they acquire from savers to purchase corporate debt .

Government Securities

In the book, U.S. government securities are categorized as long-term debt instruments and are a major component of the broader category of capital market instruments. These instruments, which have original maturities of one year or greater, serve as essential vehicles for the long-term channeling of funds from lender-savers to borrower-spenders.

Characteristics and Purpose

U.S. government securities are issued by the U.S. Treasury to finance the deficits of the federal government. Within the larger context of capital market instruments, they are distinguished by several key features:

- Liquidity: They are the most liquid securities traded in the capital market because they are the most widely traded bonds in the United States. The book notes that the daily volume of transactions for these securities often exceeds $500 billion.

- Risk Profile: Like all capital market instruments, they experience wider price fluctuations than short-term money market instruments. However, they are often used as the benchmark for “default-free” bonds when calculating the risk premium of other instruments, such as corporate bonds.

- Holders: These securities are held by a wide array of entities, including the Federal Reserve, commercial banks, households, and foreigners.

U.S. Government Agency Securities

The book identifies a closely related category within capital market instruments: U.S. government agency securities.

- Issuers: These are long-term bonds issued by various government agencies, such as the Government National Mortgage Association (Ginnie Mae), the Federal Farm Credit Bank, and the Tennessee Valley Authority.

- Function: They are used to finance specific sectors or items, such as mortgages, farm loans, or power-generating equipment.

- Guarantee: Many of these agency securities are guaranteed by the federal government and function similarly to U.S. Treasury bonds in terms of who holds them.

Role in the Financial System

In the broader overview of the financial system, these securities are vital for the efficient allocation of capital. Because of their high liquidity and perceived safety, they are frequently used in both direct finance, where they are sold directly to lenders, and indirect finance, where they are held by financial intermediaries like insurance companies and pension funds that require certainty regarding future fund availability. Furthermore, the Federal Reserve utilizes these securities as a primary tool for conducting open market operations to influence the monetary base and interest rates.

Financial Intermediaries

In the book, financial intermediaries are defined as institutions that borrow funds from people who have saved and, in turn, make loans to people who need funds. These institutions are the cornerstone of indirect finance, which is the primary route for moving funds from lender-savers to borrower-spenders in the financial system.

The Role of Financial Intermediation

The process of indirect finance using intermediaries, known as financial intermediation, is essential because it reduces the frictions that otherwise hinder the efficient movement of capital. The book emphasizes that while the media often focuses on securities markets (direct finance), financial intermediaries are actually a far more important source of funding for businesses. They perform three critical functions:

- Reduction of Transaction Costs: Small savers are often frozen out of financial markets because the time and money spent on transactions are too high. Intermediaries reduce these costs by utilizing economies of scale (such as using a single legal contract for thousands of loans) and specialized expertise.

- Risk Sharing: Intermediaries engage in asset transformation, where they create and sell assets with risk characteristics that investors find comfortable and use the proceeds to buy riskier assets. They also facilitate diversification, allowing individual savers to hold a collection of assets to lower their overall risk exposure.

- Management of Asymmetric Information: Intermediaries mitigate the problems that arise when one party lacks sufficient knowledge about the other. They are experts at screening potential borrowers to reduce adverse selection before a transaction and monitoring them to reduce moral hazard afterward.

Categories of Financial Intermediaries

The book classifies financial intermediaries into three main categories based on their primary sources and uses of funds:

- Depository Institutions (Banks): These include commercial banks, savings and loan associations, mutual savings banks, and credit unions. They are unique because they accept deposits, which are a major component of the money supply.

- Contractual Savings Institutions: These include life insurance companies, fire and casualty insurance companies, and pension funds. Because they acquire funds at periodic intervals on a contractual basis, they can focus on long-term investments like corporate bonds and mortgages.

- Investment Intermediaries: This group includes finance companies, mutual funds, money market mutual funds, and hedge funds. While investment banks share the name, the book distinguishes them as a different type of intermediary that helps corporations issue securities rather than taking in deposits to make loans.

Regulation and Soundness

Because of their vital role and the risks posed by asymmetric information, financial intermediaries are among the most heavily regulated sectors of the economy. Government regulation aims to increase information available to investors and ensure the soundness of these institutions to prevent financial panics, where doubts about one institution lead to widespread withdrawals across the entire system.

Transaction Costs

In the book, transaction costs are defined as the time and money spent in carrying out financial transactions. These costs represent a major obstacle for individuals with small amounts of excess funds, as they can effectively freeze them out of financial markets. For example, the book notes that an individual wanting to lend $1,000 to a productive entrepreneur might find that the legal fees to draft an airtight contract exceed the interest they would earn, making the transaction unprofitable.

Financial intermediaries play a vital role in the financial system because they are specifically structured to reduce these transaction costs, thereby allowing small savers and borrowers to benefit from financial markets. The book identifies two primary ways intermediaries achieve this:

- Economies of Scale: This is the reduction in transaction costs per dollar of investment as the size (scale) of transactions increases. By bundling the funds of many small investors together, an intermediary can take advantage of lower costs. For instance, a mutual fund can purchase large blocks of stocks or bonds, spreading the brokerage commission over many investors. Similarly, a bank can hire one specialized lawyer to produce a standard loan contract used for thousands of loans, reducing the legal cost per individual transaction to just a few dollars.

- Expertise: Financial intermediaries develop specialized expertise that allows them to further lower costs and provide additional benefits to their customers. For example, their expertise in computer technology enables them to offer liquidity services, which are services that make it easier for customers to conduct transactions. These services include providing checking accounts that pay interest while allowing depositors to pay bills conveniently.

By utilizing these methods, financial intermediaries ensure that funds are channeled to those with productive investment opportunities, which is essential for a well-functioning and efficient economy.

Risk Sharing

In the book, risk sharing is described as a fundamental benefit provided by financial intermediaries, made possible by their ability to maintain low transaction costs. This function is a core part of the “indirect finance” route, where institutions stand between lender-savers and borrower-spenders to facilitate the flow of funds.

The Process of Risk Sharing

The book explains that financial intermediaries share risk through several key mechanisms:

- Asset Transformation: Intermediaries create and sell assets with risk characteristics that investors find comfortable. They then use the funds acquired from these sales to purchase other assets that may carry significantly higher risk. This process is referred to as “asset transformation” because risky assets are effectively turned into safer assets for the public.

- Earning on the Spread: Intermediaries earn a profit by managing the “spread” between the higher returns they receive on risky assets and the lower interest or dividend payments they make on the safer assets they have issued to savers.

- Diversification: The book defines diversification as investing in a collection (portfolio) of assets whose returns do not always move together, resulting in a lower overall risk than that of individual assets. Intermediaries use their low transaction costs to pool many different assets into a new, single asset which they then sell to individuals, allowing small savers to achieve a level of risk reduction that would be too expensive to manage on their own.

Significance within the Financial System

Risk sharing is one of the three primary reasons the book identifies for the dominance of indirect finance over direct finance (the other two being the reduction of transaction costs and the management of asymmetric information). By providing these services, financial intermediaries allow small savers and borrowers to participate in and benefit from financial markets, which is essential for an economy to reach its full potential.

The book also notes that the ability to share and transform risk is a key driver for specific types of intermediaries; for example, mutual funds allow shareholders to hold more diversified portfolios than they otherwise could, while insurance companies manage financial hazards by pooling premiums to pay out benefits when specific disasters occur.

Asymmetric Information

In the book, asymmetric information is defined as a situation in which one party in a financial transaction possesses insufficient knowledge about the other party to make accurate decisions. This imbalance of information is a primary reason why financial intermediaries (such as banks, insurance companies, and mutual funds) play such a vital role in the economy, often proving more important than securities markets for getting funds to borrowers.

Asymmetric information leads to two specific problems: adverse selection and moral hazard.

Adverse Selection: The “Before” Problem

Adverse selection occurs before a transaction takes place. In financial markets, it refers to the fact that potential bad credit risks (those most likely to produce an undesirable outcome) are often the ones who most actively seek out loans.

- The Role of Intermediaries: Financial intermediaries address this through screening. For example, a bank becomes an expert in producing information about firms or individuals, sorting good credit risks from bad ones before lending funds.

- Avoiding the Free-Rider Problem: While private companies can sell information to help investors distinguish between good and bad firms, they often suffer from the “free-rider problem,” where non-payers use the same information as payers, driving prices to their true value and eliminating the profit incentive to produce the information. Intermediaries avoid this by primarily making private loans rather than buying traded securities, ensuring they alone benefit from the information they produce.

Moral Hazard: The “After” Problem

Moral hazard arises after a transaction occurs. It is the risk that a borrower will engage in activities that are undesirable from the lender’s point of view because they make it less likely that the loan will be repaid.

- The Role of Intermediaries: Intermediaries mitigate this through monitoring and the enforcement of restrictive covenants. For instance, venture capital firms often place their own people on a new business’s board of directors to keep a close watch on activities and earnings, ensuring managers act in the interest of the owners (solving the “principal-agent problem”).

- Asset Transformation: Intermediaries also engage in asset transformation, creating safer assets for the public while they themselves hold riskier assets, earning a profit on the “spread” between the two by managing the underlying information risks.

Economies of Scope and Conflicts of Interest

The book notes that while intermediaries can achieve economies of scope by applying one information resource to many different services (like evaluating a firm for both a loan and a bond sale), this can lead to conflicts of interest. This specific type of moral hazard occurs when a firm has multiple objectives that conflict, potentially leading them to conceal or disseminate misleading information, which reduces the overall efficiency of the financial system.

Rationale for Regulation

Finally, asymmetric information is a core rationale for the heavy regulation of the financial system. Because depositors and creditors cannot always know if an intermediary is sound, a lack of information can lead to bank panics, where even healthy institutions face massive withdrawals. Governments implement regulations—such as mandatory disclosure, bank examinations, and deposit insurance—to increase available information and ensure the overall soundness of the financial intermediaries.

Adverse Selection

In the book, asymmetric information is defined as a situation in which one party in a financial transaction possesses insufficient knowledge about the other party to make accurate decisions. This imbalance of information leads to two major hurdles in the financial system: adverse selection and moral hazard.

Definition and Timing

Adverse selection is the specific problem created by asymmetric information before a transaction occurs. It refers to the fact that the parties most likely to produce an undesirable (adverse) outcome—the bad credit risks—are often the ones who most actively seek out loans and are, consequently, the most likely to be selected. Because adverse selection increases the probability that loans will be made to bad risks, lenders may decide not to make any loans at all, even when good credit risks are present in the market.

The “Lemons Problem” in Financial Markets

The book uses the “lemons problem” analogy to explain how adverse selection can cause markets to function poorly or collapse.

- Average Quality Pricing: If a potential investor cannot distinguish between a good firm (a “peach”) and a bad firm (a “lemon”), they will only be willing to pay a price that reflects the average quality of all firms in the market.

- Market Distortion: The owners of a good firm, knowing their securities are undervalued at this average price, will be reluctant to sell. Conversely, owners of bad firms will be eager to sell because the average price is higher than their securities are worth.

- Resulting Collapse: As good firms withdraw from the market, the average quality of available securities drops, leading investors to further decrease the price they are willing to pay. Ultimately, this can result in a market where few, if any, securities are traded.

Tools to Solve Adverse Selection

The book identifies several mechanisms used by the financial system to mitigate the effects of adverse selection:

- Private Production and Sale of Information: Private companies like Standard and Poor’s and Moody’s collect and sell data to help investors distinguish good firms from bad ones. However, this is hampered by the free-rider problem, where non-paying investors mimic the trades of those who paid for information, preventing the paying investors from realizing a profit and thus reducing the incentive for private firms to produce information in the first place.

- Government Regulation: Agencies like the SEC require firms to undergo independent audits and disclose accurate information about their sales, assets, and earnings. While this increases transparency, it cannot eliminate asymmetric information entirely, as managers still have incentives to make their firms look better than they truly are.

- Financial Intermediation: Banks become experts in screening potential borrowers. By making private, nontraded loans, banks avoid the free-rider problem because other investors cannot see or copy their lending decisions.

- Collateral and Net Worth: Lenders often require collateral (property promised if the borrower defaults) or a high net worth (“skin in the game”). These requirements reduce the lender’s losses in the event of default and ensure the borrower has a strong incentive to remain solvent, thus making the lender more willing to extend credit.

Context in Financial Crises and Regulation