Every profession has its own history, but few mirror the development of a nation as closely as accounting.

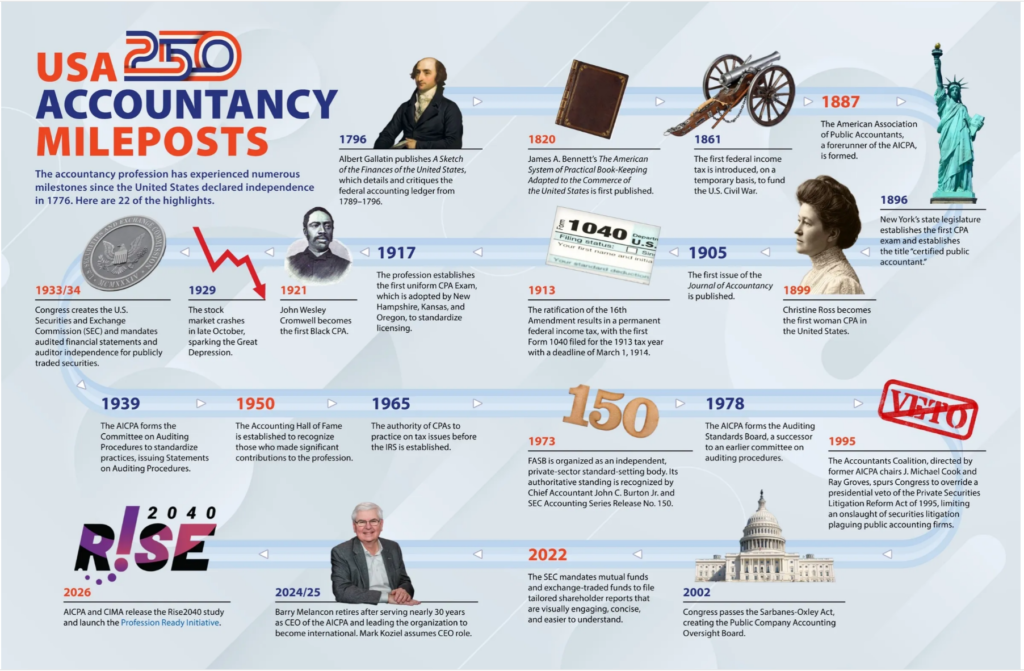

The July issue of the Journal of Accountancy features a special commemorative section celebrating the 250th anniversary of the United States by tracing the evolution of the accounting profession alongside the nation’s history. Rather than presenting accounting as an isolated technical discipline, the timeline illustrates how major developments in accounting were often responses to broader historical events—from war and industrialization to financial crises, technological revolutions, and regulatory reform.

Inspired by the infographic, I converted it into a chronological table and added an additional column highlighting the most significant U.S. or world event occurring during each respective year. My hope is that this historical context helps readers better understand why each accounting milestone mattered, not merely when it occurred.

One pattern quickly becomes apparent: accounting rarely changes on its own. The profession evolves whenever society evolves. The Civil War gave rise to the federal income tax. The Great Depression led to the creation of the SEC and mandatory independent audits. Corporate scandals produced the Sarbanes–Oxley Act and the PCAOB. Today, artificial intelligence and digital transformation are once again reshaping what it means to be an accountant.

Looking beyond accounting, the timeline also serves as a reminder of the remarkable journey of the United States over the past 250 years.

Built by immigrants, dreamers, idealists, entrepreneurs, and pioneers, the nation’s history has never been simple or without conflict. It has experienced civil war, economic depression, political division, and countless challenges. Yet throughout that journey, the United States also became the birthplace of the Second and Third Industrial Revolutions, the digital revolution, modern capital markets, many movements for civil rights, and an extraordinary amount of scientific, technological, and cultural innovation that has influenced the world.

No country is perfect, and history should be remembered in its entirety—both its achievements and its shortcomings. At the same time, it is difficult to overstate the influence the United States has had on global commerce, technology, education, popular culture, and the accounting profession itself.

Happy 250th Birthday, America🇺🇲💙🤍❤️.

May the next chapter continue to inspire innovation, opportunity, and progress for generations to come.

| Year | Accounting Milestone | Significance | Historical Context (U.S. / World) |

|---|---|---|---|

| 1796 | Albert Gallatin publishes A Sketch of the Finances of the United States | Details and critiques the federal accounting ledger from 1789–1796, representing one of the earliest analyses of U.S. government accounting. | The young United States is still establishing its financial system under the Constitution. George Washington has just completed his presidency, while Alexander Hamilton’s financial policies lay the foundation for modern federal finance. |

| 1820 | James A. Bennett publishes The American System of Practical Book-Keeping Adapted to the Commerce of the United States | The first bookkeeping textbook specifically written for American commerce, helping standardize accounting education. | The Missouri Compromise reflects America’s rapid westward expansion while temporarily easing sectional tensions over slavery during the Era of Good Feelings. |

| 1861 | First federal income tax introduced | Marks the beginning of federal income taxation, initially as a temporary wartime measure. | The American Civil War begins. Financing the war requires the federal government to dramatically expand taxation and financial administration. |

| 1887 | American Association of Public Accountants (AAPA) founded | Establishes the first national professional organization for accountants, which later becomes the AICPA. | The Gilded Age sees explosive industrial growth, railroads, and large corporations, creating demand for professional accountants and auditors. |

| 1896 | New York establishes the first CPA law and examination | Creates the Certified Public Accountant (CPA) designation and professional licensing in the United States. | America is rapidly industrializing. The Supreme Court’s Plessy v. Ferguson decision establishes the “separate but equal” doctrine during a period of major social change. |

| 1899 | Christine Ross becomes the first woman CPA | A landmark achievement for women entering the accounting profession. | The Progressive Era begins, bringing reforms in education, government, and professional standards while expanding opportunities for women. |

| 1905 | First issue of the Journal of Accountancy published | Provides a professional publication for sharing accounting knowledge, standards, and research. | President Theodore Roosevelt’s Progressive reforms strengthen government oversight of large corporations and promote corporate accountability. |

| 1913 | 16th Amendment ratified; first Form 1040 introduced | Permanently authorizes the federal income tax and establishes the modern U.S. tax filing system. | The Federal Reserve System is also established, fundamentally reshaping America’s financial and banking system. |

| 1917 | First uniform CPA Examination established | Standardizes CPA licensing across multiple states, improving consistency and professional competency. | The United States enters World War I, greatly increasing the need for standardized financial reporting and government accountability. |

| 1921 | John Wesley Cromwell becomes the first Black CPA | A milestone for diversity and inclusion within the accounting profession. | The Roaring Twenties begin, characterized by economic prosperity, technological innovation, and expanding business activity. |

| 1929 | Stock Market Crash | Exposes weaknesses in financial reporting and corporate oversight, setting the stage for sweeping regulatory reform. | The Great Depression begins, causing widespread unemployment, bank failures, and economic collapse. |

| 1933–1934 | Congress creates the SEC and mandates independent audits for publicly traded companies | Establishes the foundation of modern securities regulation and external auditing in the United States. | President Franklin D. Roosevelt’s New Deal introduces broad financial reforms designed to restore investor confidence after the Depression. |

| 1939 | AICPA forms the Committee on Auditing Procedure | Begins issuing Statements on Auditing Procedure (SAPs), standardizing auditing practices nationwide. | World War II begins in Europe, accelerating industrial production and increasing demand for reliable financial reporting. |

| 1950 | Accounting Hall of Fame established | Honors individuals who have made lasting contributions to the accounting profession. | America enters the postwar economic boom, becoming the world’s dominant industrial and economic power. |

| 1965 | CPA authority to practice before the IRS established | Officially recognizes CPAs’ authority to represent taxpayers before the Internal Revenue Service. | President Lyndon B. Johnson’s Great Society programs significantly expand the federal government’s fiscal responsibilities through Medicare, Medicaid, and social programs. |

| 1973 | Financial Accounting Standards Board (FASB) created | Establishes an independent private-sector organization responsible for U.S. GAAP. | The Oil Crisis, Watergate, and economic stagflation heighten demands for corporate transparency and credible financial reporting. |

| 1978 | AICPA forms the Auditing Standards Board (ASB) | Creates the primary body responsible for developing U.S. auditing standards for nonpublic companies. | Increasing globalization and multinational business operations require more sophisticated and consistent auditing practices. |

| 1995 | Private Securities Litigation Reform Act enacted | Limits certain securities litigation against public accounting firms while balancing investor protection. | The Internet era begins transforming business, financial markets, and information technology, fueling rapid economic expansion. |

| 2002 | Sarbanes–Oxley Act (SOX) creates the PCAOB | Represents the most significant reform of corporate governance and auditing since the 1930s. | Following the Enron, WorldCom, and other accounting scandals, Congress restores investor confidence through sweeping regulatory reforms. |

| 2022 | SEC modernizes shareholder reporting for mutual funds and ETFs | Requires reports to become more concise, visually engaging, and accessible for investors. | In the aftermath of the COVID-19 pandemic, regulators increasingly emphasize digital communication, transparency, ESG reporting, and investor accessibility. |

| 2024–2025 | Barry Melancon retires; Mark Koziel becomes CEO of AICPA & CIMA | Marks a major leadership transition for the accounting profession’s largest organization. | Artificial intelligence rapidly enters mainstream business, while the profession faces talent shortages and accelerating digital transformation. |

| 2026 | Rise2040 study and Profession Ready Initiative launched | Positions the accounting profession for an AI-driven future through workforce development and modernization. | As AI, automation, cybersecurity, and data analytics reshape every industry, accounting evolves from transaction processing toward strategic advisory, technology, and continuous learning. |

— Linden Lake

Leave a Reply